Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

August Home Maintenance Tips

Maintaining your home can sometimes feel like a daunting task, but with a few proactive steps, you can keep it running smoothly and efficiently. Regular maintenance not only preserves the functionality of your home but also enhances its safety and energy efficiency. Here are some essential home maintenance tips to help you stay on top of things:

Test and Maintain Water Heater Efficiency: Sediment buildup in your water heater can reduce its efficiency. Drain the tank to remove sediment, check the temperature setting, and inspect for any leaks or signs of wear to ensure it operates efficiently and safely.

Check and Clean Bathroom Exhaust Fans: Bathroom exhaust fans help remove moisture and prevent mold growth. Clean the fan blades and grills, and ensure the vent is functioning properly to maintain good air quality.

Inspect and Replace Weather Stripping on Doors: Worn or damaged weather stripping can lead to drafts and energy loss. Inspect and replace it around doors to improve energy efficiency and maintain a comfortable indoor temperature.

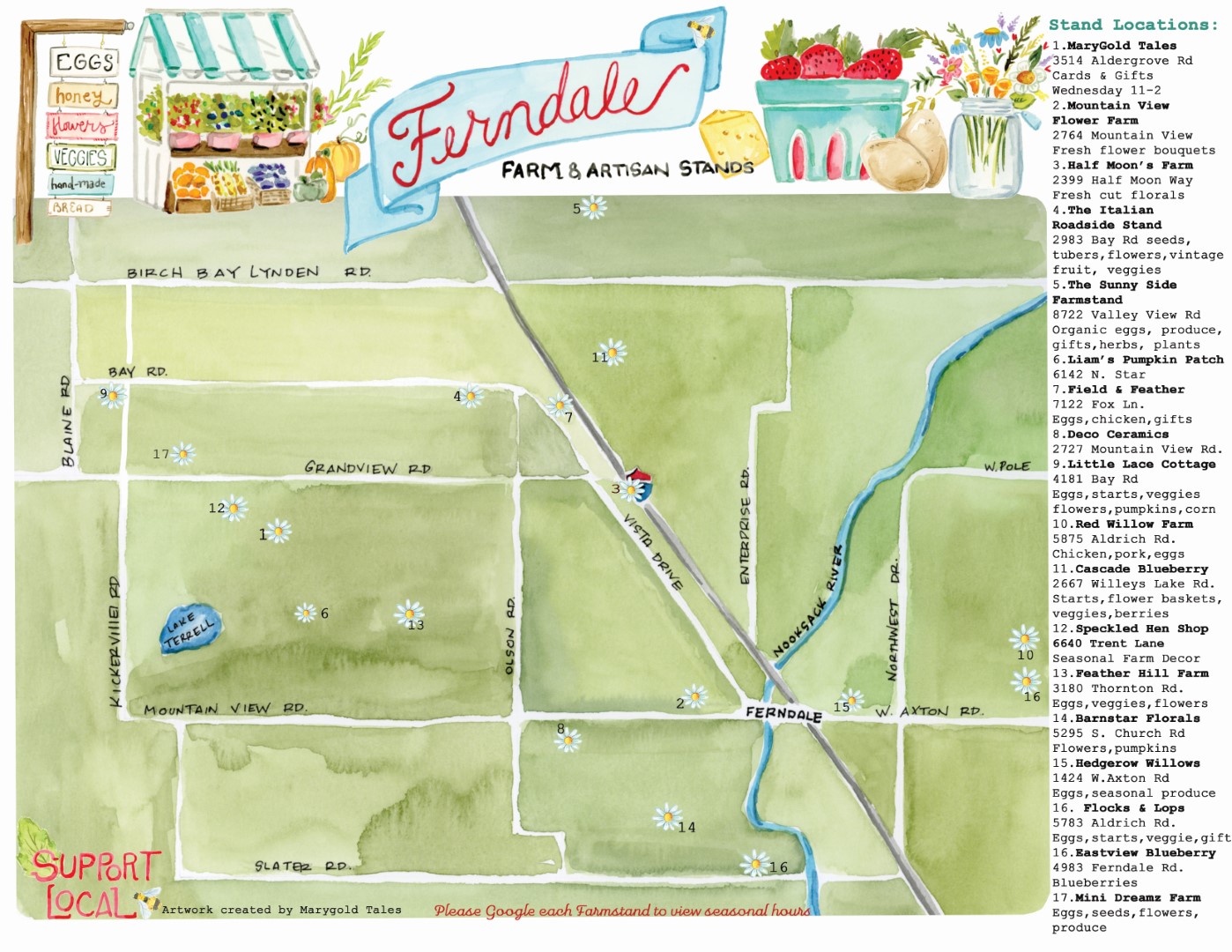

Find a Farmstand with MaryGold Tales

Many of you have received a custom home illustration from us as a memento of your home you sold after closing. These illustrations were created by the amazing local artist Mary from MaryGold Tales, just for you!

Mary is a vibrant presence in her community and wanted to find a way to bring together all the small businesses and farms in her area and share them beautifully with the community. She has created the map (seen above) to highlight each of these businesses.

She continuously updates the map, adding more incredible businesses each month. To be a part of the map or to join her mailing list to receive the updated map each month, sign up on her website. More details are in the link below!

1 Year Anniversary

It’s hard to believe that it’s already been a year since we joined forces. We’ll be honest, it wasn’t all easy. Real estate agents are independent contractors and merging two independent people together presents challenges. We’ve had hard conversations, we’ve cried, but we’ve also had the most fun we’ve ever had in real estate, and we’ve always affirmed each other in our strengths. We’ve grown, and are so proud of ourselves and what we’ve accomplished. This job is deceptively lonely. Even though we’re around people all the time, most of the business moments are alone. Working together has given us a support we’ve both craved for a long time. We’ve used our different personalities as a strength and our clients benefit from that. We love working together and we love working together for our clients. It’s been the best thing we could’ve done and we’re excited for year two!

Together, we’ve:

Closed over 40 transactions, including

—helping 28 clients find their dream home

—helping 14 clients get their house sold for their next adventure

and counting…

Cheers to us!

July Real Local Feature

WIDNOR FARM

Ryan and Brianna, alongside their 3 young (+ wild) kiddos, operate Widnor Farms, a livestock ranch in Custer, WA. Their family raises forested pork, dry aged angus beef & pastured poultry as well as seasonal lamb. With the passion of bridging the gap between farm and consumer, they opened their online store in 2019, selling individual cuts of meats to their customers across the greater Seattle area. But, in 2021, they made the leap to open an in person store right on the ranch where customers can not only purchase the food to feed their family, but they can connect with where it all comes from. “There is something special about purchasing your meats at the ranch store, while seeing the livestock live such happy lives in the pastures nearby. We wanted people to experience that deep connection with their food that we get everyday.” Brianna’s popular instagram page, @widnorfarms, gives their customers a back seat to their daily chores, silly kids antics and farming practices used on their regenerative ranch. In 2023, Widnor Farms also began a chefs prepared food line, bringing you ready to eat meals featuring local ingredients and paired with Widnor Farms proteins. In 2024, after 2 years of building and planning, they also opened their own on farm small craft butchery that brings more sustainability to the food production landscape of Whatcom County. Want to check it out for yourself? Visit the ranch store in Custer on Saturdays from 10-2PM or shop online at www.widnorfarms.com and have your proteins brought right to your door!

1858 W Badger Road

Custer, WA 98240

Website: www.widnorfarms.com

Email: brianna@widnorfarms.com

Phone Number: 360.941.0935

Instagram: @widnorfarms

![]()

BEACH BUNGALOW – Birch Bay, WA

Reservations & Information

3 Beds | 1 Bath | Sleeps 6

Kick back and relax in this calm, stylish space located walking distance to the beach. The home is a brand new space with all new furnishings. Enjoy cooking dinners in the stylish kitchen and a fire or yard games in the backyard.

The home is bungalow style. Each bedroom has a queen size bed. Everything in the home is brand new comfortable

And stylish. The third bedroom is accessed from the outside and has its own keypad entry.

July Home Maintenance Tips

Ensure a safe and enjoyable summer at home by tackling a few maintenance tasks. A little effort now means a safer and more enjoyable season ahead.

Check and Clean Dryer Vents: Lint buildup in dryer vents can be a fire hazard. Clean out the vent pipe and the area around the dryer to ensure it operates safely and efficiently.

Test and Maintain Smoke and Carbon Monoxide Detectors: Ensure that all smoke and carbon monoxide detectors in your home are functioning properly. Replace batteries if necessary and test the alarms to ensure they are operational.

Inspect and Maintain Decks and Patios: Check for loose boards, nails, or screws in your decks and patios. Clean and reseal wood surfaces to protect against moisture and sun damage, ensuring they remain safe and looking good throughout the summer.

Cascade Best Winner

I am honored and grateful to be voted as the Best Real Estate Broker (Bronze) and Best Commercial Broker (Gold) in the 2024 Cascade Best awards. Your trust and support are invaluable, and I am incredibly thankful for the opportunity to serve such a wonderful community. This recognition is a testament to the collaborative effort and trust we’ve built together.

It is pretty funny that I won for the Commercial Real Estate category because commercial is definitely not my specialty. I do have so many of you friends involved in the business community in Whatcom County that ask for help with your commercial real estate needs. l’m thankful to have Jeff Hopwood, the man responsible for getting me into real estate in the first place to work with my clients who have Commercial Real Estate needs. I’m honored to be involved with those transactions, and am always confident that Jeff has the knowledge and expertise to make big things happen for my people in Commercial Real Estate!

Accolades motivate me to continue striving for excellence, delivering exceptional service, and helping you achieve your real estate goals. Thank you for your confidence in my work and for being an integral part of this achievement. Your support means the world to me, and I look forward to continuing to working together in the future!

NAR Settlement Update

As promised, here is the latest update regarding the $418 Million NAR Lawsuit Settlement and how it will affect real estate operations in WA State. As the deadline to opt in to the NAR Lawsuit Settlement approaches, the Northwest Multiple Listing Service (NWMLS) announced last week that they have voted to NOT opt-in to the settlement.

The NWMLS is a member-owned organization that serves over 35,000 brokers in WA State where 26 of the 39 counties in WA, including Snohomish, King, Skagit, Kitsap, Whatcom, and Pierce counties share their listings. Unlike many MLSs across the country, the NWMLS is not owned by the National Association of Realtors (NAR), giving them a choice to opt in to the lawsuit settlement which would require payment and adhering to specific business practices. With transparency a proven cornerstone of their mission, the NWMLS felt secure and confident in the structure and processes they have in place. Their intent has always been to elevate consumer protection and provide an open and fair marketplace, which led to the decision to not opt in to the settlement agreement.

Besides payment, there are 4 major mandates resulting from the settlement agreement that NAR-owned MLSs and non-NAR MLSs that opt in will be required to adapt to in August 2024.

- The requirement to provide Buyer Brokerage Compensation (BBC) in all listings will be removed.

- Brokers will be required to enter into a written Buyer Agency Agreement (BAA) with Buyers which clearly outlines compensation before rendering Buyer Brokerage Services.

- Listing Agreements will de-couple the listing brokerage compensation from the buyer brokerage compensation, outlining clear and separate offerings of compensation for each side of a transaction.

- MLSs will be prohibited from publishing offers of buyer brokerage compensation.

The majority of the requirements mandated by the settlement had already been established by the NWMLS. In 2019, the NWMLS removed the BBC requirement and started to syndicate the published BBCs to third-party sites, such as Zillow, for full consumer transparency. In 2022, the listing agreement was amended to reflect de-coupled compensation and the BBC was added to the front page of the Purchase and Sale Agreement (PSA). In Jan 2024, WA State law was put into place requiring all brokers to enter into BAAs, which are called Buyer Brokerage Service Agreements (BBSAs) in WA. This legislative change was enacted with support from the NWMLS who advocated for the new laws and they re-built their forms to support this elevated level of transparency.

The NWMLS was able to choose to opt in, which would require payment towards the settlement and adhering to the fourth process change of removing published BBC from listings on the database. Due to the NWMLS’s historical innovation and leadership surrounding representation, compensation, and transparency, which has been an example for the rest of the country, they voted to not opt-in. In fact, they concluded that not publishing an offered BBC, whether the offering is zero, a flat rate, or a percentage, would reduce consumer transparency.

Further, not publishing what a seller is offering or not offering, could lead to deceptive practices that could harm consumers. The NWMLS shared this in their press release announcing their decision:

NWMLS will not “opt-in” to NAR’s proposed settlement agreement. NWMLS’s rules and forms, together with the revised Agency Law, provide for consumer-friendly brokerage relationships. Sellers negotiate how much to compensate the listing firm and decide whether to offer to contribute toward the buyer’s broker compensation and the amount of any such offer. Buyers agree how much to pay their own brokers at the outset of their relationship, and can then negotiate for the seller to help cover that cost as part of the purchase.

NAR’s proposed settlement agreement largely duplicates the rules and practices in place in NWMLS’s service area for several years – with one notable exception. The settlement agreement eliminates compensation transparency for buyers and restrains sellers’ choice by prohibiting sellers from making offers of compensation through the MLS. Instead, the settlement agreement allows for offers of compensation “off MLS”, where that information is hard to find and not available to all buyers and brokers. That change is a step in the wrong direction and is detrimental to consumers and brokers alike.

NWMLS strives to provide consumers with all relevant information about a listed property to promote efficiency, competition, and an open and free market. NWMLS’s rules and forms broaden, not limit, consumer choice and do not favor any brokerage service model or compensation structure. NWMLS allows the market to operate unimpeded by MLS rules.

NAR’s removal of compensation transparency from the MLS pushes consumers and brokers to make secret deals “off-MLS”, inviting deceptive practices, discrimination, and unfair housing. Depriving buyers of information about the transaction risks harming buyers, especially those buyers who are already disadvantaged, including first-time home buyers and members of protected classes. Of course, prohibiting offers of compensation in the MLS also unnecessarily restrains the seller’s choice and absolute right to offer compensation to a brokerage firm representing the buyer.

As I move forward in my business practices and adhere to the NWMLS leadership, I am proud to be a broker in WA State. Our corner of the world has put great thought, effort, and execution towards elevating the consumer experience in a real estate transaction. We have navigated changes, tackled open communication head-on, and strive to bring value to the consumer at every turn. This lawsuit has created a lot of noise and confusion; it is important to understand how WA stands out from the rest of the nation.

As headlines soar and the media bends the narrative, you can count on me to help keep you informed so you can accurately grasp how the progression of the industry affects you. I am happy to report that how we are conducting business here will be in line with the innovation that the NWMLS already has in place. We will watch the rest of the country catch up and proudly lead that charge. Stepping out in front seemed bold at first, and has proven to be the right course of action. Due to the insightful, considerate, and thoughtful guidance of the NWMLS, we will continue to prioritize full transparency and be able to focus on providing the best service possible for our clients.

If you have any additional questions or want to discuss this topic, please reach out. It is always my goal to help keep my clients well-informed and empower strong decisions. Here’s to moving forward with excellent practices in place to help consumers safely and securely buy and sell property.

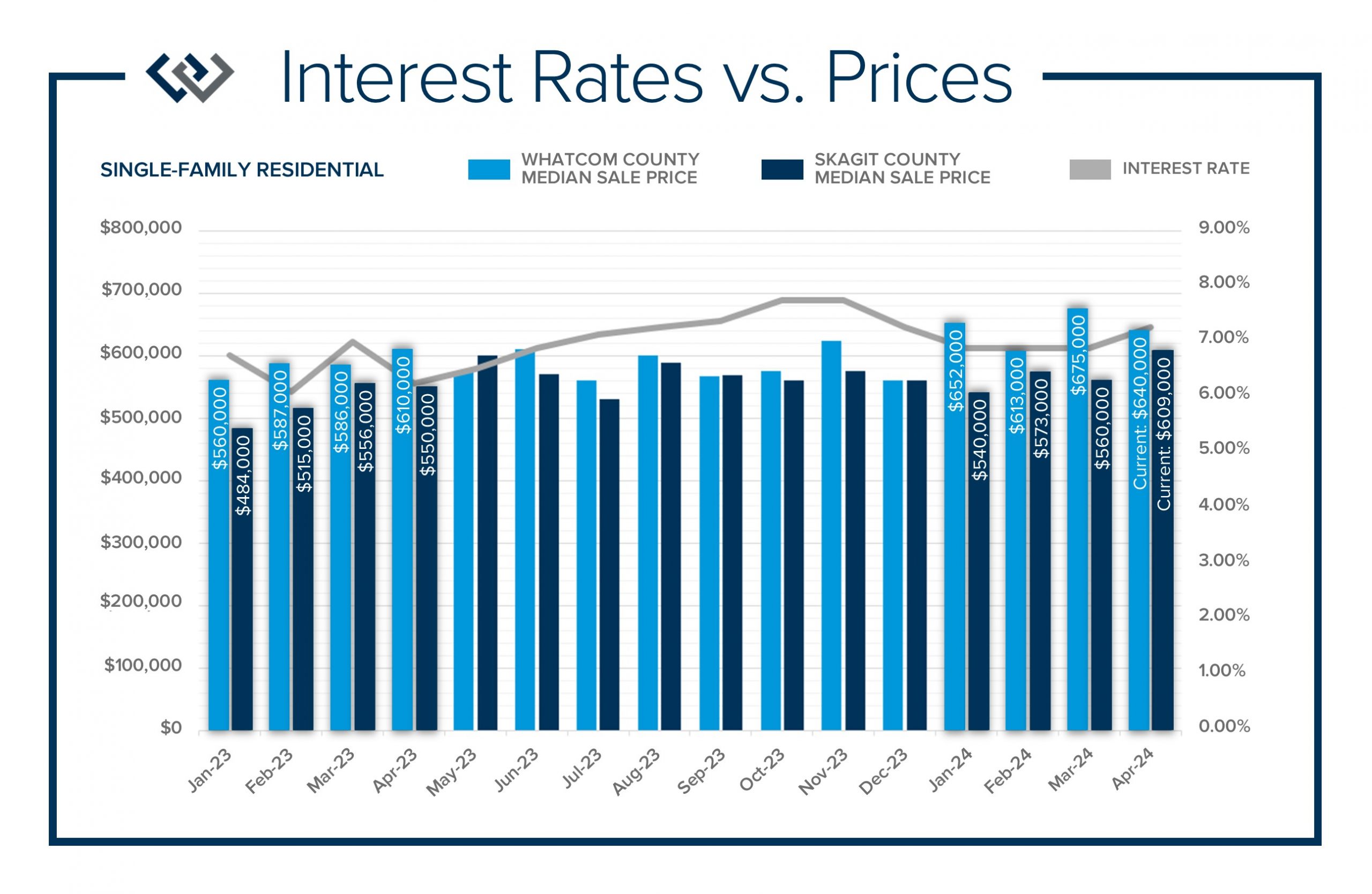

Spring 2024 Insights and Trends

As we sit almost five months into 2024 in the middle of the spring market and I reflect on how the year is going, I am grateful, amazed, and locked in on the stats. You see, the last four years since the start of the pandemic have been an eventful and wild ride. 2020 saw a brief halt in sales when the shelter-in-place order went into effect, and once protocols were established to make real estate essential, the market started to take off. Many people utilized that time to re-evaluate where they wanted to live, whether that meant in a different state, from an urban location to a rural setting, or from a shared condo building to a single-family residential house.

This re-organization of where people wanted to live was coupled with historically low interest rates that hovered in the 3% range, leading to the highest number of recorded closed sales in 2020 and 2021 that we had seen in over a decade. All of this activity took place while inflation was on a stubborn uphill trajectory, causing the Fed to make some big rate increases to help combat consumer spending in 2022.

Rates increased by three percentage points from February 2022 (3.9%) to October 2022 (7%) and have remained in that higher range ever since. This quickly put a stall on buyer demand as monthly payments quickly became more expensive, putting downward pressure on affordability. This caused a correction in prices from the peak in spring 2022 to the first quarter of 2023 when prices bottomed out.

In Whatcom County, prices corrected from the peak to the bottom by 15%, and in Skagit County, 17%. Prices started to bounce back from the bottoming out in the spring of 2023, and since then have increased 15% in Whatcom County and 26% in Skagit County. While prices were stabilizing and then growing from Q1 2023 until now, interest rates have hovered in the 7% range. Buyer demand slowly regained its footing throughout 2023 and when the calendar turned to 2024, buyers started to come out in force despite the interest rates never returning to historic lows. It is safe to say that many buyers have accepted the higher interest rates as the new normal.

In this new normal, monthly payments are high as prices remain stable and have had extreme appreciation since the start of 2024. In Whatcom County, prices have grown by 14% from Dec 2023 to April 2024 and in Skagit County by 9%. At the end of 2023, it was reported that the average homeowner had at least 62.4% home equity in Whatcom County and 61.6% in Skagit County. That equity measurement doesn’t include the price growth we have experienced so far in 2024.

Rates have remained stubborn due to inflation still being a challenge. Inflation has tempered, but not to the 2% year-over-year level the Fed wants to see before easing interest rates. The Fed met at the beginning of May and indicated that rates will slowly come down in the second half of 2024 and into 2025 if inflation rates reach that 2% year-over-year mark. That will be a key marker to track as the Fed Chairman, Jerome Powell has made it clear that will be what it takes to cause rate relief.

Some buyers may wait to enter the market once rates have eased, and many are jumping in now as they are happy to secure today’s prices. Demand will only increase when rates improve, which should most likely cause additional price growth. Creative financing options such as interest rate buy-downs and ARM (Adjustable-Rate Mortgage) loans have helped buyers manage their monthly payments when making a purchase. The key factor I help the buyers I serve stay focused on, is the affordability of their monthly payments.

This focus has proven to be the most productive and strategic number to stay connected with to help a buyer remain confident and effective. Buyers often make adjustments in price point, features, and/or location to match up a manageable monthly payment with the home they buy. Analyzing the trends, stats, and values from one area to the next is an exercise that helps buyers gain clarity. We often say that when a buyer finds a home that matches 75-85% of their criteria they are in striking distance to make an offer. In a seller’s market like this, buyers must make compromises to succeed.

A bright light for buyers is that we have seen a recent jump in new listings. There were 36% more new listings in April 2024 over April 2023 in Whatcom County and 26% more in Skagit County. With seller equity so high and pent-up seller motivation boiling over, we are finally starting to see additional inventory come to market. We are still experiencing tight inventory, but it is growing. This is providing some additional selection and should hopefully continue throughout 2024.

Continuing my daily, weekly, monthly, and annual commitment to studying the market is a benefit to the clients I serve. Understanding how inventory, rates, and prices all relate to each other helps me provide valuable insights for clients so they can appropriately strategize when they want to enter the market. These trends vary from one city to the next, in different price points and property types. If you are curious about how today’s trends relate to your real estate goals, please reach out. Further, if you know someone who needs my assistance, please direct them my way. It is my goal to help keep my clients well-informed to empower strong decisions.

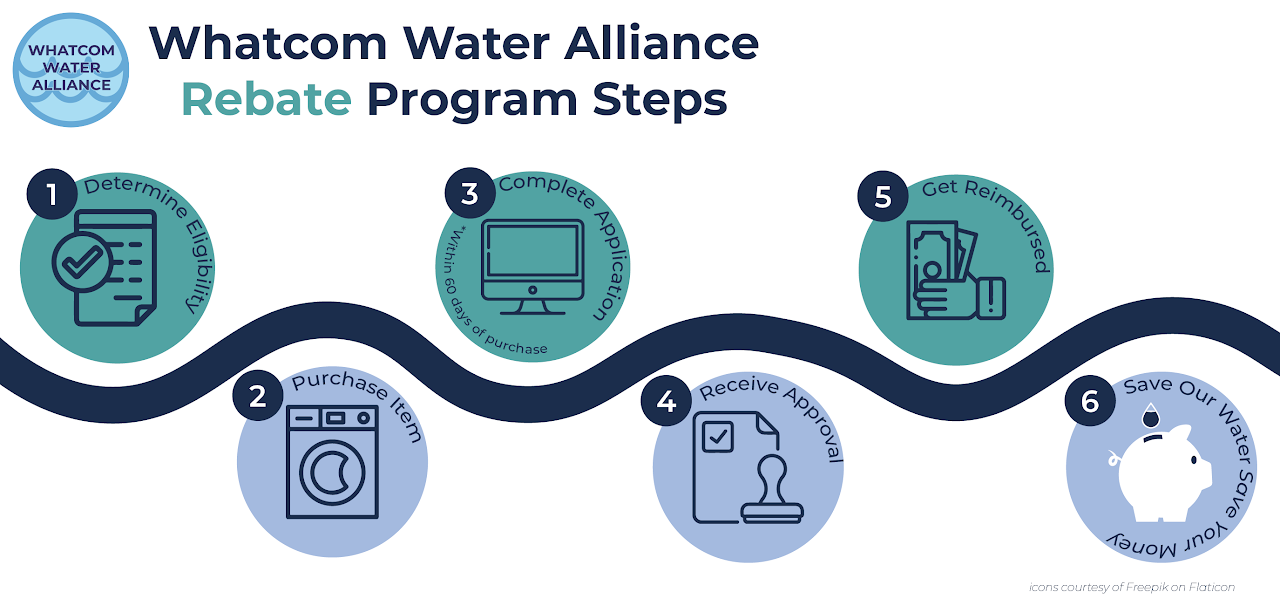

Water Conservation Rebates

Water conservation rebates are available to all Whatcom County single family homes that do not reside within City of Bellingham city limits. If you plan to make any upgrades to your home, check to see if your new appliance or system has an Energy Star or WaterSense logo, and you may be eligable for one of these rebates!

Rebates Available:

High Efficiency Toilets - Up to $100 Rebate

Irrigation Controllers - Up to $75 Rebate

High Efficiency Clothes Washer - Up to $100 Rebate

City of Bellingham water customers can find rebates through the City's Water Use Efficiency Rebate Project page.

June Home Maintenance Tips

Get your home ready for a beautiful summer with these home maintenance tips! From ensuring your outdoor spaces are in top shape to keeping your indoor systems running smoothly, a little upkeep goes a long way. By addressing these tasks, you can keep your home in great shape and enjoy a worry-free summer.

- Check for Pest Activity: With the arrival of warmer weather, pests such as ants, termites, and rodents become more active. Inspect your home for signs of pest activity, such as droppings, chewed materials, or entry points. Seal any cracks or holes and consider hiring a pest control professional if you notice an infestation.

- Maintain Your Lawn and Garden Equipment: Ensure your lawnmower, trimmer, and other garden tools are in good working condition. Sharpen blades, change the oil, and clean the equipment to keep them operating efficiently. Properly maintained tools make yard work easier and more effective.

- Inspect Plumbing for Leaks: Check your home’s plumbing system for any leaks or drips, especially in areas that are not frequently used, such as basements or crawl spaces. Look for water stains, mold, or mildew, and repair any leaks promptly to prevent water damage and high water bills.

{kind=link}