Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Returning to Normal

There is no doubt that 2022 has been one of the most eventful years in real estate. This is saying a lot coming off the record-breaking years of the pandemic. We will probably never see anything like 2020 and 2021 again. During this time the market responded to a historical event that motivated the rearrangement of our communities due to societal shifts all while we had the lowest interest rates ever. It was a doozy of a time! Demand was spurred by the option to work from home; buyers craved the perfect space to be at home and cheap money made these moves plentiful. The market had a slight pause at the onset of the pandemic in the spring of 2020 and then it took off like a freight train. Heightened demand, cheap money, and low inventory caused prices to increase at the most significant rate we have ever seen. How was this train barreling down the tracks going to slow down? The speed at which this train was moving was not safe or sustainable. The only way to stop it was an increase in interest rates.

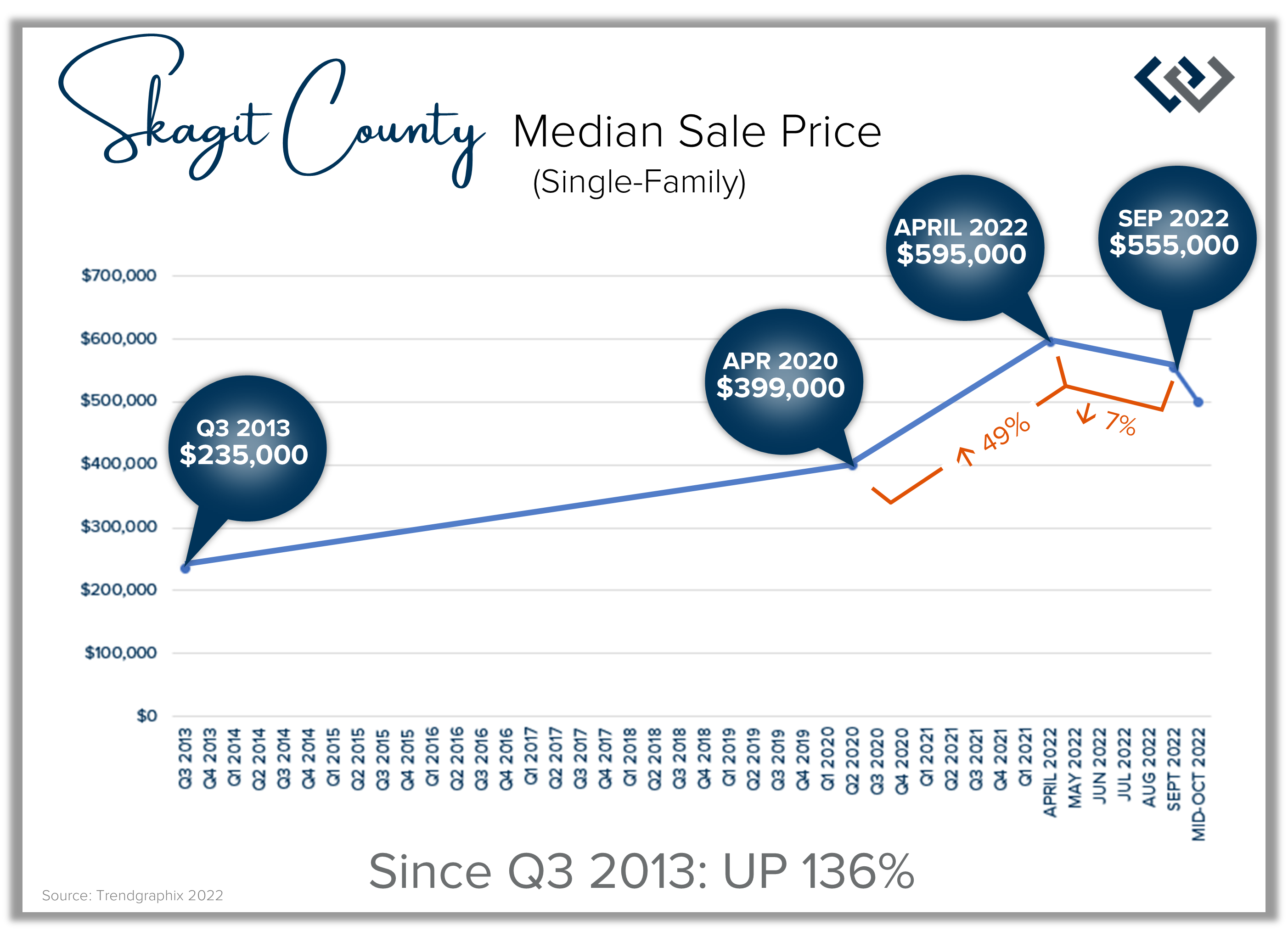

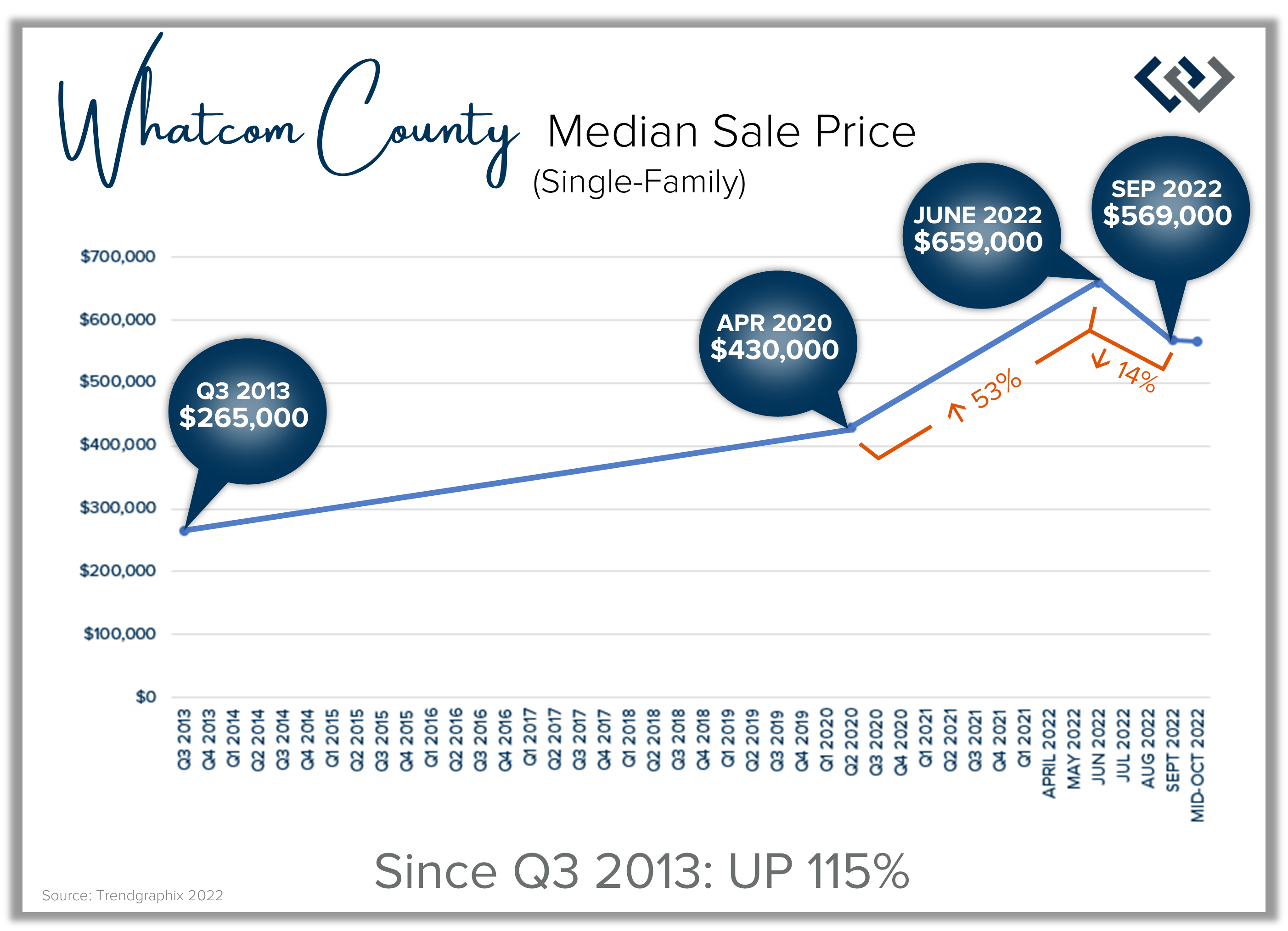

In Whatcom County, from April 2020 to the peak (June 2022) prices grew by 53%, and in Skagit County, from April 2020 to the peak (April 2022) prices grew by 49%. Bear in mind that historical norms for annual price appreciation are 3-5%, making this two-year time period unlike any other! The Fed needed to make the cost of borrowing money more expensive in order to slow down inflation. This was applicable to the entire economy, not just real estate, causing short-term rates to increase for credit cards, car loans, and lines of credit, as well as long-term mortgage rates.

Since the peak, interest rates have increased by 1.5% and this has put downward pressure on prices and slowed demand. There is a rule of thumb in our industry called the 1/10 rule: for every 1-point change in interest rates, buying power shifts by 10%. For example, if a buyer is pre-approved for a $600,000 purchase at a rate of 5.5% and then the rate increases by 1-point to 6.5% in order for the buyer to have the same monthly payment they must decrease their purchase price by 10% to $540,000. This rule applies when rates go down too, which led to the fierce increase in prices over the pandemic years.Buyers most often make buying decisions based on the monthly payment and it is no wonder that the new interest rate environment has caused prices to decrease. As you can see from the graph, prices in Whatcom County are down from the peak by 14% and down in Skagit County by 7%, which very much reflects the 1/10 rule, as rates went from 5% on average in April to 6.5% in September. Month-to-date this October, prices in Whatcom County are only slightly down over September prices and are down a bit more in Skagit County.Expect home prices to adjust based on rate increases, decreases, or stabilization based on the 1/10 rule, not because the sky is falling. Buyers that bought at or around the peak need to keep the faith and understand that real estate is a long-term hold investment with the average homeowner spending at least 8 years in their home. A correction in the market is solved with time and most likely these buyers secured their homes with very low debt service making their payments lower to help them sustain this adjustment. The Fed’s plan is working to slow down the train and help us return to a more sustainable market.While interest rates are higher than they have been they are still lower than the 30-year average of 7.5% and prices are coming off the peak, but not crashing. In Whatcom County, prices are up 32% from April 2020, and in Skagit County, they are up 39%. Most importantly, long-term price growth since Q3 2013 is up by 136% in Whatcom County and up 115% in Skagit County. In fact, more than 50% of homeowners in WA state have at least 50% equity in their homes making them prepared to make a move when their life-needs will motivate a change. Keeping all of this in perspective will lead sellers to successful moves with a calm understanding of our new normal after an unprecedented time in history. Buyers are enjoying an increase in selection and more time to make their buying decisions. They now have time to discern these big life changes and to analyze the financial aspect of a move versus needing to make a decision in a 15-minute showing appointment before a home was gobbled up in multiple offers. They are also afforded the opportunity to do further due diligence on the properties they are interested in and negotiate contract contingency terms that protect them throughout the transaction. It is also not uncommon for work orders that a buyer has called out to be added to a contract. We are seeing the occasional multiple offers on homes that are special and priced perfectly, so aligning with a broker who can identify value and opportunity is key so a buyer doesn’t miss out. Another important aspect for a buyer to consider is the set-up of their financing terms. With rates higher than they have been and the age-old strategy of managing monthly payments always in play, creative financing options such as rate buy-downs and ARMs (Adjustable Rate Mortgages) are additional options to consider when looking at the overall financial picture of making a purchase. Make sure the broker you work with has a collection of reputable lenders that can provide options as each lender will have different programs to choose from. We are even seeing sellers pay credits on behalf of buyers to buy their rate down in order to make the monthly payment more attainable. The negotiations we are seeing in this market are being dictated by buyer affordability which requires collaboration. Since most sellers have large amounts of equity, we have seen successful meeting-of-the-mind solutions to create win-win outcomes for both sides. As the market comes into balance we are seeing more of a give-and-take and the importance of navigating these changes is critical. During these times when a market shifts, the cream rises to the top. The listings that are well prepared for the market and priced appropriately will be the winners. Cutting corners and overpricing will lead to frustration and loss. Sellers need to seek out trusted advisors who can properly analyze the new market conditions, bring perspective to their goals, keenly negotiate, and assist them in showcasing their home in the best light possible. Buyers need to align with a professional who understands current market values, can negotiate with data and rapport, assist them in their lending options and help create win-win outcomes. Brokers like this are not the norm. We are coming off of two years of trying to hold onto a speeding train and now we have the opportunity to steer it through expertise. Expertise is earned and I could not be more passionate about helping my clients navigate the new normal with the tools and experience I bring to the table. I am invested in my clients’ goals and strive to empower strong decisions through thorough research, sound counsel, and clear advocacy. Please reach out if you are curious about how today’s market matches up with your goals or if you know someone I can help.

Affordable Travel through Timeshare Ownership

A few weeks ago my family went on our annual Florida vacation, but this year it looked and felt very different. The timeshare we own was unfortunately destroyed by Hurricane Ian only two weeks before our scheduled vacation. My grandparents bought this condo in the 80’s and gifted the weeks they owned to their grandchildren when they were no longer able to go. I inherited my week after spending many years vacationing there as a child. I now take my children to that same place every year because we only have to pay the dues (less than $600/year) as our lodging expense.

As it is tradition, we still wanted to go this year despite our condo being destroyed but needed to find a different place to stay. Have you looked into how much it costs to stay ON THE BEACH in Florida?! I had not until this year and was shocked. We ended up in St. Pete Beach and BOY WAS IT EXPENSIVE. We won’t be doing that again! I am hopeful our Condo Association will be able to rebuild- although I am sure it will be at least two years until we are able to go back. My point here is, because we own a week we are able to enjoy a 1 bedroom condo that sleeps 6 with a kitchen on the beach and pools for 13% of the cost of renting a similar unit.

During Covid we also decided to buy into a timeshare in Lake Chelan. We own 3 weeks that rotate throughout the months every year. We don’t go all 3 weeks each year, so we are able to rent one or more of them and cover the cost of ownership! There are so many benefits to timeshare ownership and affordable travel is just one.

Below is a simple breakdown of the different types of timeshares. There are even more options than these 3, some with blends of different ones and each having their benefits and drawbacks.

Deeded Timeshare

A deeded week timeshare means that the owner literally gets a deed for their week and they own it. It is commonly called fee simple in real estate terms. Since it is a deeded week, the owner has the option to sell their timeshare, rent it out and give it away if they wish to. Deeded week timeshares were the most common when timeshares originated. There are still timeshares like this available but many companies have moved away from deeded weeks in favor of flexibility. (This is the type we own in Florida.)

Right To Use Timeshare

Right to use timeshares do not come with a deed, but they do come with a contract stating how long the owner has the right to use the timeshare. Most right-to-use leases are over after 30-99 years depending on what is specified in the original agreement. However, owners can still sell their ownership to somebody else on the resale market.

Leasehold Timeshare

Leasehold timeshares are not owned in perpetuity and have a specific expiration date. They do however hold the same benefits and rights as other timeshares. Disney Vacation Club is the most prominent example of a leasehold timeshare.

There isn’t really a benefit to me financially to share my passion for Timeshare Ownership with you all. I just LOVE travel and being able to travel affordably means that I can travel more. And who doesn’t want to travel more?! If you want to learn more or look into timeshare ownership I’d love to grab a coffee or a beer and dream with you!

2023 Real Estate Goals

The new year is just around the corner! If you are thinking you might want to invest or make a move next year let’s talk!

My calendar is open starting in November for some afternoon/evening consultations. Let’s meet at the brewery of your choice or I can come to your home. We can do some dreaming and draw out a timeline for your goals. It’s never too early to start!

CLICK HERE to schedule a time to chat. I can’t wait to meet with you!

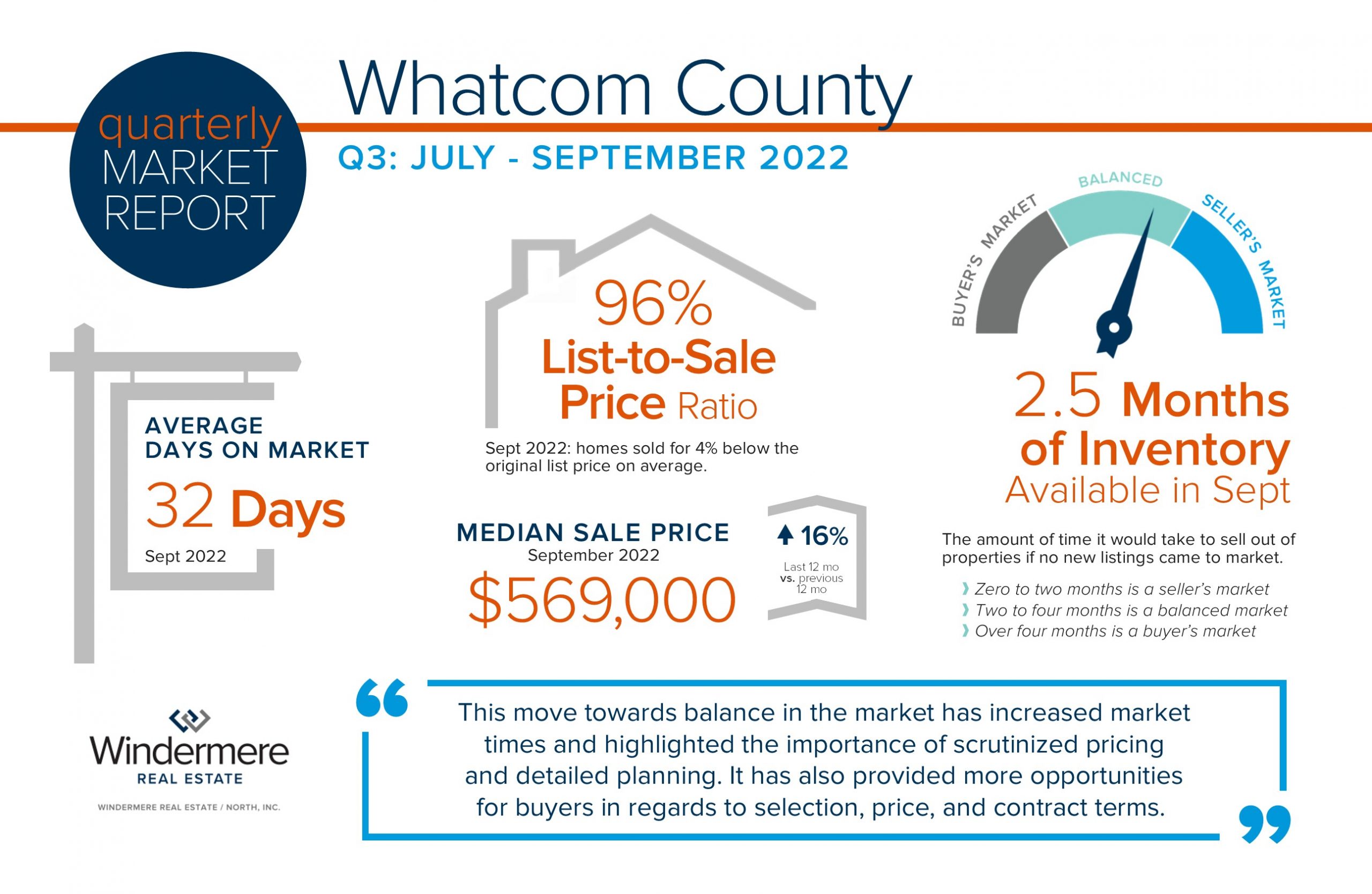

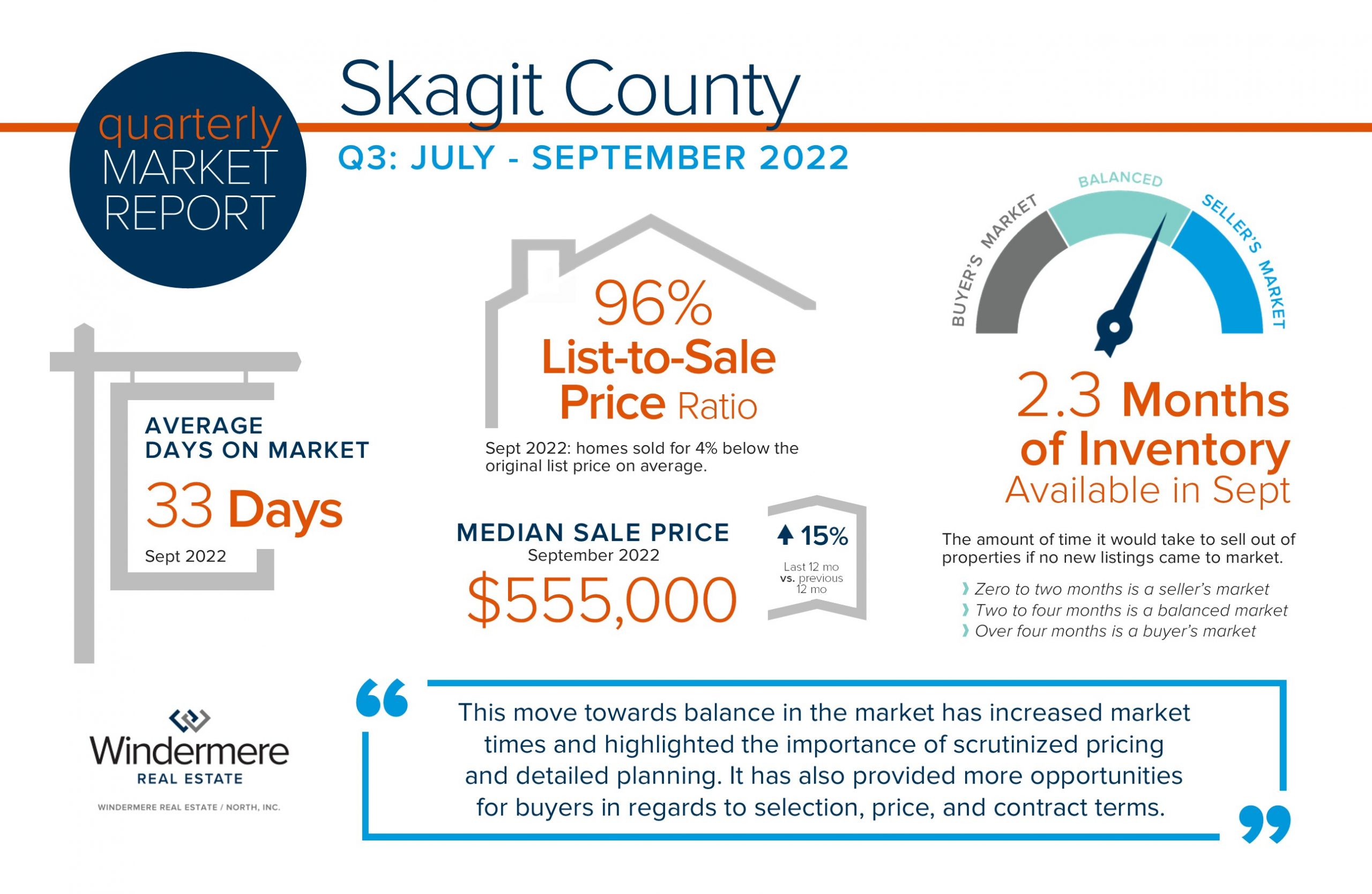

QUARTERLY REPORTS Q3 2022

The real estate market is adjusting to new environmental factors as we round out 2022. Interest rates have been on an upward trend since the spring and have increased by 2 points since the first of the year. This has put downward pressure on the peak prices we saw in the spring as we return to more normalized, historical rates. We must keep in perspective the strong year-over-year price gains as these environmental factors settle out. Additionally, we are sitting on top of 10 years of price growth resulting in over 50% of homeowners in WA state with at least 50% home equity.

The real estate market is adjusting to new environmental factors as we round out 2022. Interest rates have been on an upward trend since the spring and have increased by 2 points since the first of the year. This has put downward pressure on the peak prices we saw in the spring as we return to more normalized, historical rates. We must keep in perspective the strong year-over-year price gains as these environmental factors settle out. Additionally, we are sitting on top of 10 years of price growth resulting in over 50% of homeowners in WA state with at least 50% home equity.

This move towards balance in the market has increased market times and highlighted the importance of scrutinized pricing and detailed planning. It has also provided more opportunities for buyers in regards to selection, price, and contract terms. This market requires keen analytical skills, strategic negotiations, creativity, and a higher level of customer care.

I welcome the balance and normalization and look forward to helping my clients make moves to match their needs in life! Please reach out if you are curious about how the market relates to your goals or know someone that needs my help.

Make A Statement With Your Front Door

We all know about curb appeal, but did you know that your door color might influence how much a buyer offers on your home? A recent study showed that certain door colors could impact the value of your home by thousands of dollars.

Here are a few fun facts. Blue and black were the most popular choices: buyers said they would offer around $1,537 more for a home with a slate blue door. $6,449 more for a home with a black door. Olive green doors also showed a small increase in offer price. Not all colors were received positively, for example buyers said they would offer roughly $6,516 less for a home with a pale pink door.

This is just one example of how small changes, like the color of your door, could be a decision maker for some buyers. If you’re thinking of selling, changing the color of your door may be a good idea. I’d be happy to share my recommendation with you!

Fall Activates & Pumpkin Patches

Autumn is finally in the air which means time for cider sipping, pumpkin patches, hay rides and corn mazes! Don your favorite fall attire and get ready for a season of fun and all the pumpkins you can carry at these local farms! Check out my favorite part of each one below:

WHATCOM COUNTY

STONEY RIDGE FARM ~ Best : Kids Educational

2092 VanDyk Road – Everson

October | Fridays 12-5 |Saturdays 10-5

BELLEWOOD FARMS ~ Best: Apple Picking

6140 Guide Meridian Rd- Lynden

Wednesday- Sunday | 9am- 4 pm

WILLETTA FARMS ~ Best: Farm Animals

1945 E Badger Rd- Everson

October | Fridays 10am-1pm | Saturdays & Sundays 10am- 5 pm

SKAGIT COUNTY

SCHUH FARMS ~ Best: Array of Activities

15565 WA-536 – Mt Vernon

October | 9 am- 6 pm Daily

GORDON SKAGIT FARM ~ Best: Unique Pumpkin Variety

15598 McLean Rd – Mount Vernon

October | 9am to 6pm | Daily

JONES CREEK FARMS ~ Best: U-pick Fruit

32260 Burrese Rd- Sedro Woolley

Friday- Monday | 10am- 5pm

I can’t wait to hear which ones you visit!

Prepare Your Home for The Changing Seasons

We’re more than half way through September, which means fall is just around the corner! No matter how you feel about the impending seasonal change, I hope this list helps you prepare your home for fall and winter.

- Wash textiles: curtains, throw blankets, washable pillow covers

- Shake out your rugs

- Clean the gutters

- Clean your windows

- Clean the fireplace

- Test run the furnace

- Replace/clean filters: furnace, water, washing machine, dishwasher

Summer Food Drive Update

| Thank you to everyone who donated to our summer food drive! We collected 924 pounds of food and $2,700. Collectively, we’re helping our neighbors in need with over 2,000 meals. The Volunteers of America Western Washington shared with us how grateful they are for this, as the need is high due to the rising costs of groceries.Thank you!

|

Current Shift In Inflation & Interest Rates

It has been my goal to report to you accurate, real-time updates on the real estate market as we navigate the shift that started in May 2022. The two factors that have been the biggest contributors to this shift are inflation and interest rates. Inflation caused interest rates to rise by over 2-points over a 5-month period. When rates hit and then crested the 5% mark in mid-April is when we started to see sales slow and create downward pressure on prices.Since mid-April, we saw rates jump another point and crest 6% in late June. This has caused a correction in price appreciation or what is called a deceleration in price growth. While we have come off the peak prices of the Spring of 2022, year-over-year price appreciation is still very strong, and long-term price growth is historical! In Whatcom County, prices are up 19% when you compare the last 12 months of price growth over the previous 12 months of price growth, we like to call this complete year-over-year price appreciation. In Skagit County, prices are up 16%. These percentages are well above average and will end the year still well above the historic complete year-over-year average of 3-5% annually. This is the perfect illustration of a price correction due to market influencers such as inflation and interest rates. Here’s the good news, July inflation numbers were reported at 8.5% which came off the June peak of 9.1% which has caused interest rates to start to stabilize. Rates have come down off the peak in late June and have been hovering in the 5%. This caused July pending sales to increase over June indicating consumers becoming more comfortable with this new normal. In Whatcom County, pending sales are up 22%, and in Skagit County up 28%.

Also bear in mind there is a difference between short-term and long-term mortgage rates. Mortgage rates are dependent on long-term interest rates and home equity lines of credit, car loans and credit cards are dependent on short-term interest rates. There is a lot of talk in the news about rising rates and how they are being used to combat inflation. This has applied more towards short-term rates as the Fed would like consumers to slow their spending that utilizes short-term rates to temper inflation. In fact, the last increase in short-term rates actually caused long-term mortgage rates to lower.

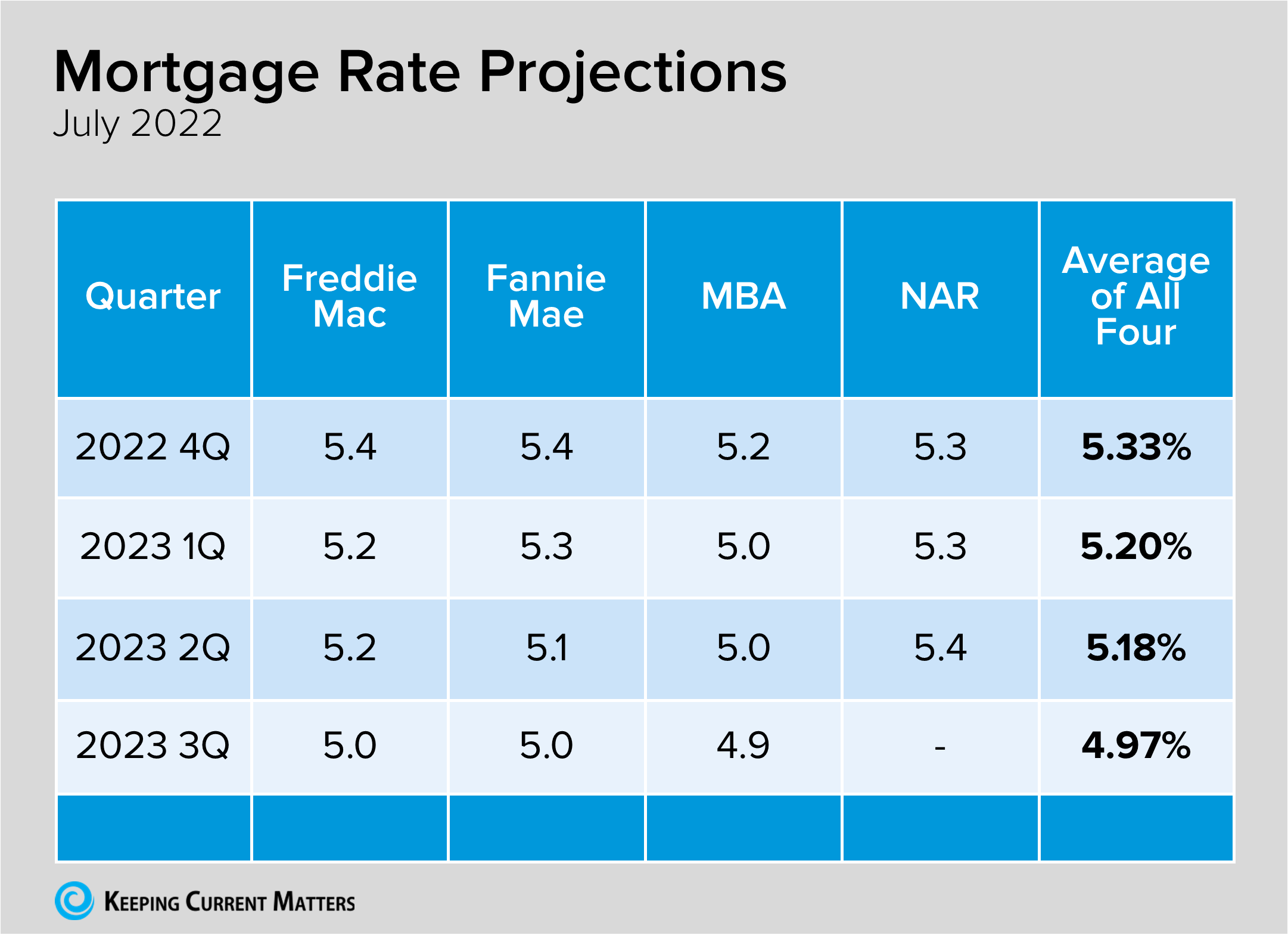

Below, you can check out a video released by Matthew Gardener, Windermere’s Chief Economist addressing the rate of inflation, how it relates to interest rates, and where we are headed as we finish out 2022. This video was actually released a few weeks back and it is proven to be spot-on. We are fortunate at Windermere to have Matthew’s guidance. It is always my goal to help keep you well informed and empower strong decisions. Please reach out if you are curious about how today’s market relates to your real estate and financial goals.

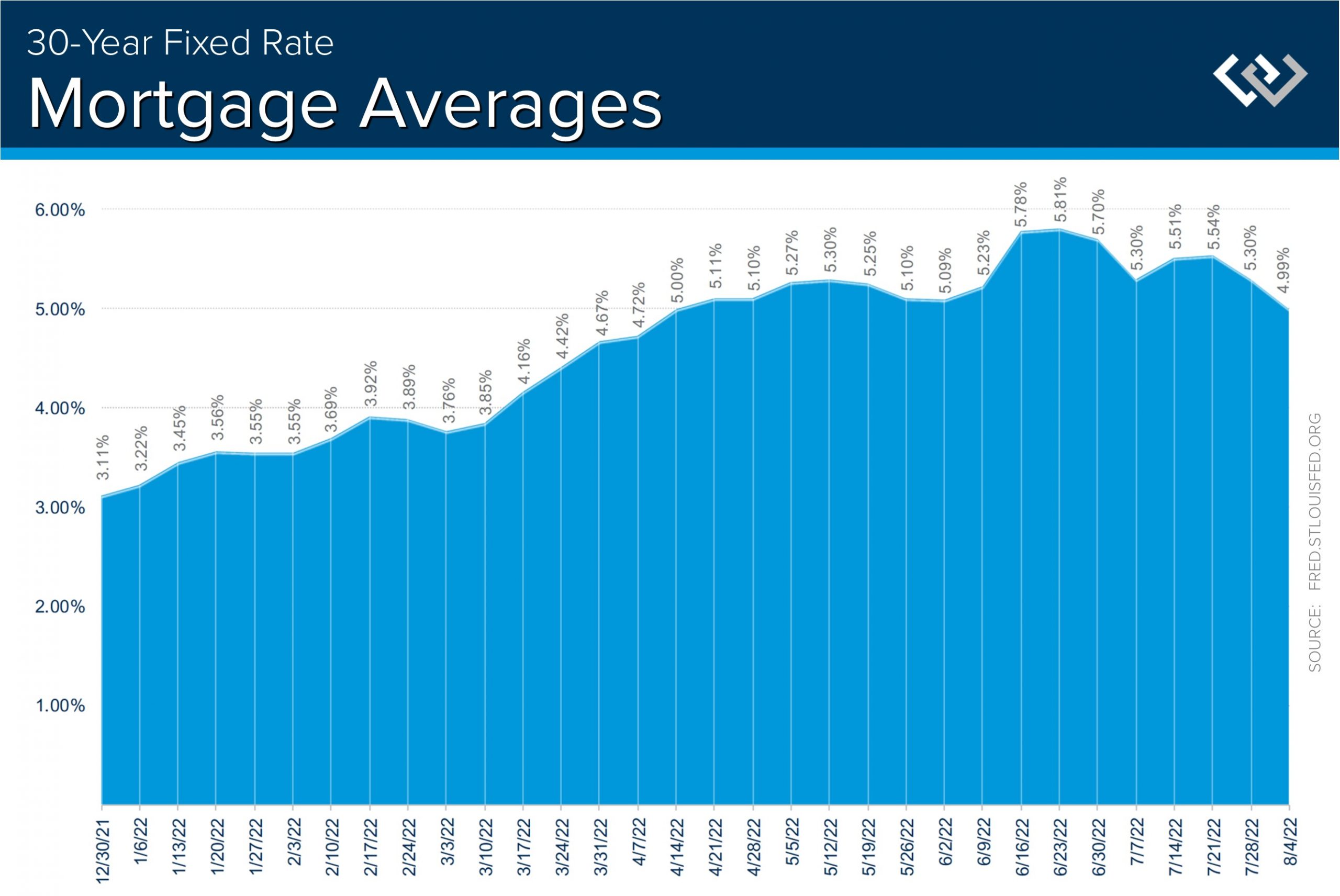

Shifting Market: How Interest Rates Affect Prices

As we continue to examine the shift in the market, we must take a moment to take a deep dive into interest rates. Since the first of the year, long-term interest rates have increased 2.7% from 3.11% on 12/30/21 to the peak of 5.81% on 6/23/22, but have started to level out. On 8/4/22 rates found themselves at 4.99% which provided more opportunities for buyers and helped increase demand. These are the base rates that are released but can shift up based on the loan program or elements in the buyer’s application, like a credit score.

You see, affordability has been a challenge with the incredible price appreciation we have seen over the last two years. The median price is up 48% ($430,000 to $635,000) from July 2020 to July 2022 in Whatcom County and up 32% ($420,000 to $555,000) in Skagit County. Average annual price gains are typically 3-5% making these last two years a time of significant growth. This is on top of 10 straight years of positive price growth. Homeowners are sitting on a ton of equity!

These recent extreme price escalations were directly connected to the historically low interest rates that were in the 3-4% starting in the spring of 2019 and lasted until the spring of 2022. To combat inflation the Fed made the move they’ve been talking about for some time and started to raise interest rates. This started to take shape in April, peaked in June, and has now started to stabilize as we head into the dog days of summer. As rates start to normalize it is putting downward pressure on the peak prices. Bear in mind that the average interest rate over the last 30 years is around 7.5% which we are well below. This low-rate environment was also coupled with a scarcity of inventory and now we are starting to see more selection and a shift from a sellers’ market (0-2 months of inventory) to a balanced market (2-4 months of inventory).

Buyers often choose their price point based on the monthly payment they will need to sustain throughout the term of their loan, not necessarily the highest price they are qualified for. If you look at the chart below you can easily see what buyers are needing to consider financially and how that would price them out of the higher price points. That has directed the demand to adjust to lower price points in order to provide a monthly payment that is sustainable and affordable. Hence, putting downward pressure on the peak prices we saw in spring 2022 when rates were in the 3-4% and there was only 1 month of available inventory in Whatcom and Skagit counties. Now there is 2 months of available inventory for both counties, which is an indicator of a balanced market.

The sky is not falling, we are just adjusting to the new normal of interest rates and getting used to having additional selection and competition. Prices are still up significantly year-over-year and homeowners are sitting on a mound of equity built over the last decade. Prices have come off the peak of April 2022, but are starting to recalibrate in relation to the cost of debt service. We anticipate this correction to level out in the coming months. Experts are predicting rates to simmer in the 5% with the hopes of not entering into the 6% like we saw in June as the volatility of this adjustment was finding its way as a response to inflation.

It is also important to understand that mortgage rates are long-term rates and when you hear in the news that the Fed is going to hike interest rates to combat inflation, that it is often short-term rates they are referring to such as car loans, credit cards, and home equity lines of credit. The point of the short-term rate hikes is to get people to slow their spending and save more to hedge against inflation. In fact, the last short-term rate hike caused long-term mortgage rates to lower. Make sure you are consulting an expert and not just listening to the media.

I will continue to keep a close eye on rates, prices, and inventory so my clients are equipped with the most up-to-date information. We must understand all three of these elements are directly connected to each other and they will adjust and find balance. Our local job market is strong, home equity is high, interest rates are still well below the 30-year average, and there is a lot that is motivating the economy. While we may be experiencing a recession, we are not experiencing a dismal housing market. Sales are maintaining at the same level as 2018 and 2019 which were very strong years in real estate, but a bit less than the pandemic-fueled years of 2020 and 2021 that saw a reorganization of our communities due to the work-from-home phenomenon.

Real estate has always been a long-term hold investment and also the place you call home. It must be looked at from a financial perspective and a lifestyle one as well. We are starting to see some creative options in the market with rate buy-downs, even seller credits, and some buyers opting for ARMs (adjustable rate mortgages) in order to get the payment that works for them. Please reach out if you have questions or are curious about how your goals relate to today’s market. It is always my goal to help keep my clients well informed and empower strong decisions.