Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Which is Better, Renting or Buying?

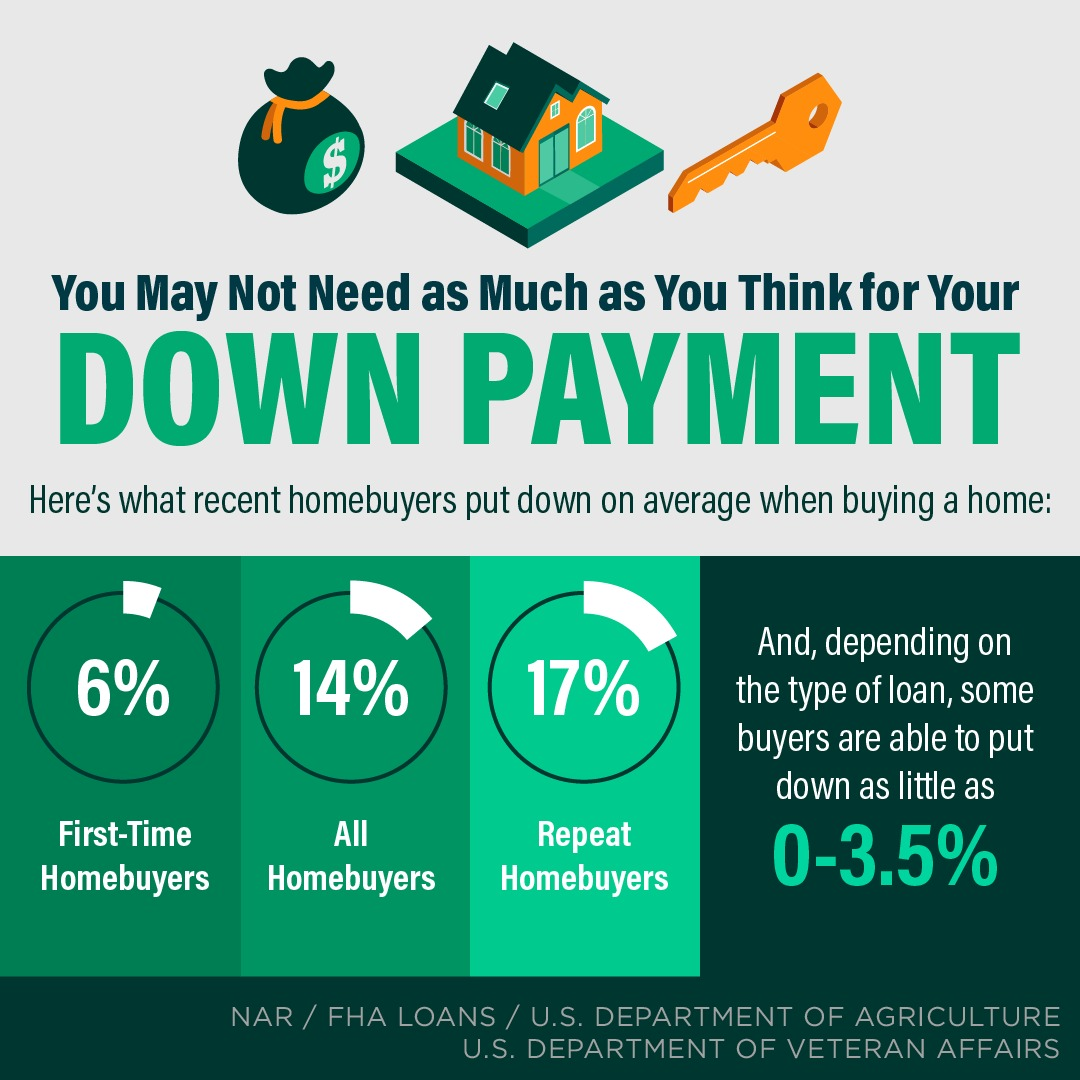

The financial benefits of owning real estate significantly outweigh the option of renting. Renting is certainly a must for some, and is what one may have to do while they build up to becoming a homeowner. Becoming a homeowner requires solid employment, good credit, and some type of down payment. Savings can all be built over time and if achieved can provide incredible long-term financial growth by becoming a down payment on a home. In fact, many people think you need a 20% down payment in order to purchase a home and that is just not the case. There are various loan programs available requiring much less than 20% down.

The financial benefits of owning real estate significantly outweigh the option of renting. Renting is certainly a must for some, and is what one may have to do while they build up to becoming a homeowner. Becoming a homeowner requires solid employment, good credit, and some type of down payment. Savings can all be built over time and if achieved can provide incredible long-term financial growth by becoming a down payment on a home. In fact, many people think you need a 20% down payment in order to purchase a home and that is just not the case. There are various loan programs available requiring much less than 20% down.

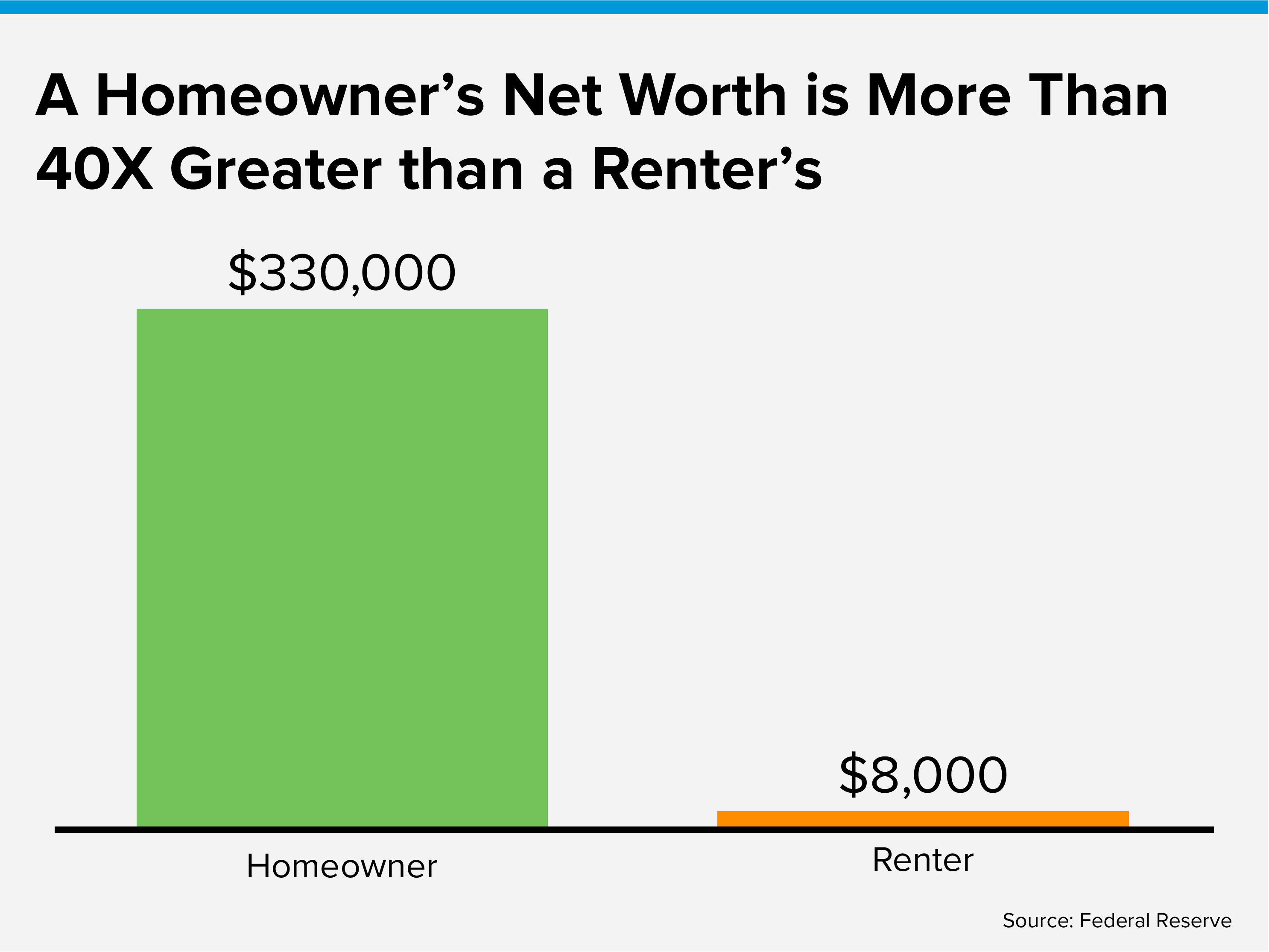

The savings of your nest egg that you would put into a home purchase is the single most powerful investment vehicle to build household wealth and financial security. Did you know that the average net worth of a homeowner is 40 times higher than one of a renter? There are many factors that play into this statistic. Take in my outline below as well as the video link below from Matthew Gardner, Windermere’s Chief Economist who also weighs in on this subject.

The savings of your nest egg that you would put into a home purchase is the single most powerful investment vehicle to build household wealth and financial security. Did you know that the average net worth of a homeowner is 40 times higher than one of a renter? There are many factors that play into this statistic. Take in my outline below as well as the video link below from Matthew Gardner, Windermere’s Chief Economist who also weighs in on this subject.

Over time, your mortgage payment becomes easier to afford. Fixed mortgage payments do not go up, but rent inevitably does. While your mortgage stays fixed your income often increases, making the monthly payment easier to handle.Real estate is a solid long-term investment. Historical home price appreciation is on your side. The historical average is 3-5%, and in some cases, that figure has been much higher. Only once, during the Great Recession, did we see multiple-year price declines. However, the people that held onto those homes since that time have been handsomely rewarded with phenomenal equity. Real estate is a long-term hold investment that provides shelter and financial opportunity. You cannot live in your stock certificate. Real estate is an investment that you can touch, feel, smell, live in, and improve! You have to live somewhere and allocate a portion of your income to shelter. Why not pay your shelter budget towards an asset that is growing for your financial future? You can also make improvements to your property that you can enjoy which will also increase the value of the asset. Diversifying your investments is important, stocks are a natural option, but real estate should be in the mix as well. I have even seen first-time buyers keep their starter home as a rental, move on to their next home and start to build their own real estate portfolio.Every mortgage payment goes towards paying down your loan principle. Right now, mortgage rates are up a bit, leading to conversations about the impact of rates. One thing I know for sure is that the interest rate on rent is 100%! None of that money ever comes back to you. Your mortgage payment goes back into your asset and becomes a forced savings account. This piles your money safely away all while your asset is appreciating year-over-year which builds long-term wealth.Owning real estate provides tax benefits. Depending on the state you live in, you can write off your real estate taxes and mortgage interest. This can offset your tax burden and save you significant money every year. There are also capital gains tax exemptions on your primary residence that you have lived in for at least two years of the last 5 years (make sure to consult your tax expert on the details). You can have tax-free gains of up to $250,000 for a single person and up to $500,000 for a married couple. This is a wonderful opportunity to move your wealth towards your future when planning for big lifestyle improvements such as retirement.I will leave you with this: it can seem overwhelming to take on the task of buying your first home or to prepare to own again after renting. Start by understanding that shopping in the price range you can afford matters. Often times people want to get their forever home right off the bat and that makes the accomplishment of becoming a homeowner much harder. Figure out how much you can afford now and put your nest egg to work sooner rather than later to start building wealth. Maybe it is a small condo that fits your budget now, but over time the money saved and the equity built can turn into the down payment needed to purchase your forever home.Owning real estate is a step-by-step journey that takes time and sacrifice. Your patience and commitment will be rewarded with compounded savings which will lead to building long-term wealth. It also creates a fond memory lane of that first condo or small house that you loved making a home, which then became the vehicle to afford the next home that better suited your lifestyle. If you are curious about the prospect of owning real estate or have a special person in your life who is poised to become a homeowner, please reach out. It is my goal to help people understand the process, align them with a trusted lender, help them make strong financial decisions, and match their living situation to their lifestyle.

2023 Economic & Housing Forecast

Thank you to all my guests that were able to join me at my Annual Economic and Housing Forecast event with Matthew Gardner, Windermere Chief Economist sponsored by Evergreen Home Loans. In case you missed it, below are my top 10 takeaways, with all of the slide information linked HERE.

BELLINGHAM METRO AREA LABOR MARKET

1. Matthew began the evening discussing jobs and unemployment. Employment rates are directly tied to housing markets so this is always a good place to start. Of the 15,500 Bellingham jobs that were lost due to the pandemic, 14,900 have been recovered….Matthew says this translates nationally to “everyone who wants to work, has a job”.

INTEREST RATES

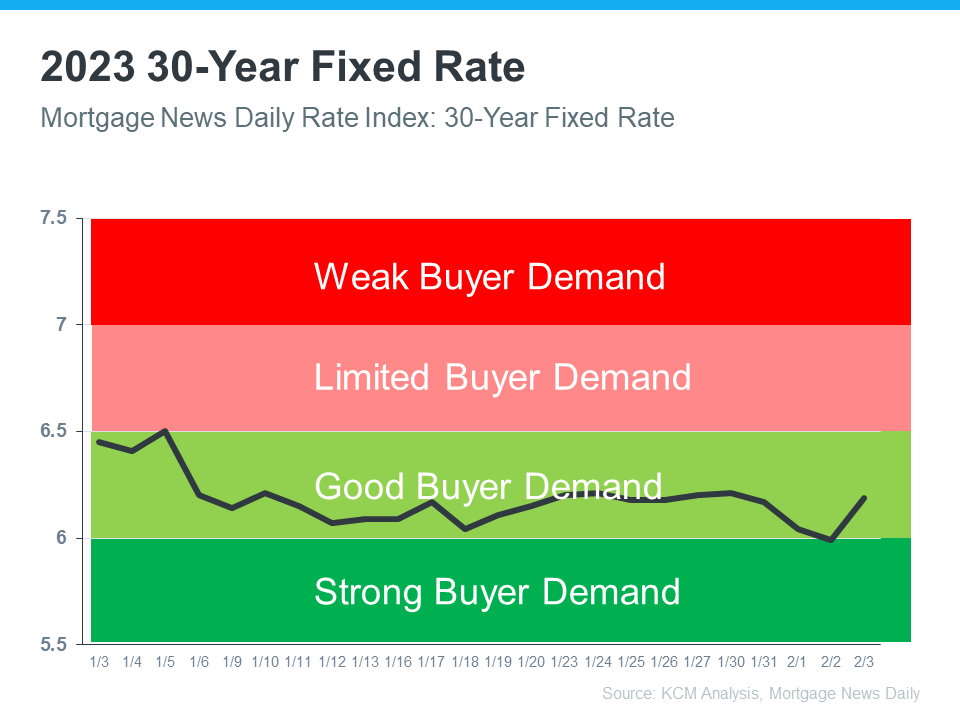

2. I know, these two words have been somewhat of a “dirty word” these past 9 months… Gone are the days of the sub-3% interest rates. They were so unheard of, Matthew even went as far as to say they were “fake.” Matthew believes that our average Mortgage rate for a 30-year Conventional Loan with be 6% for 2023 – other expert’s expectations range from 5.2 % to 6.4%, so Gardner lands pretty close to the middle.

HOUSING DEMAND

3. The increase in supply last year (due to buyer’s halting their searches when interest rates went off the charts) took us back a mere 18 moths in time. We’re still experiencing very low inventory levels in our area, hitting at about 300-400 per quarter compared to our long-term average of about 900.

MIGRATION

4. Whatcom County experienced major population growth in 2022 compared to recent years – not because of babies born (natural increase), but because of people moving to the area (net migration). I felt this in my own business and continue to have new clients every day reach out to me to move to our beautiful county from other areas.

PRICING REVERSION

5. While the average home prices have fallen in the last few months, they really are just reverting back to the long term trend, having been artificially inflated due to the extremely low interest rates.

RICH IN EQUITY

6. Right now in Whatcom County, 67.2% of homeowners have more than 50% equity in their homes. This means EVEN WITH the pricing reversion we experienced last year more than half of homeowners still have more than half the value of their mortgage balance in equity in their homes!

WHO’S MARKET IS IT ANYWAYS?!

7. As a whole in the county we are still in a Seller’s Market, we have a long time before we see ourselves in a Buyer’s Market… or will we ever? (there is a whole category in-between: the Balanced Market). When buyer demand outweighs the homes we have for sale, the number of months it will take to sell all the homes we have available quickly shrinks. This is how we determine who has the power in a market.

When I look closely at specific markets for clients some did dip into a Balanced Market over the last few months, but buyer demand is trending in a way that seems like we will be back to a strong sellers market VERY SOON, if not already, in all markets.

PRICING PREDICTIONS FOR 2023

8. Average sales price will be close to flat from 2022 for most markets… which is still SUBSTANTIALLY above 2021. Home prices in our area rose 22.7% in 2021, and up 8.8% from 2021 in 2022, and are predicted to fall just slightly at -.07% this year. That’s right… you will still have the same value you did in 2022 which is still FANTASTIC!

OVER-ALL UP

9. Only one market in Whatcom County ended the year with a LOWER median sales price from 2022 to 2021… ALL THE REST WERE UP!

HARD TO GROW

10. It has been 17 years since Whatcom County has pulled the average number of new construction building permits… Why? 26% of the cost to build here is JUST IN FEES. Not the land, not the labor, not materials… FEES!

With all this said, our biggest challenge remains AFFORDABILITY.

Let me know if you would like to dive deeper into any of these topics, or have any questions. For those of you with housing goals this year, I hope this brings you some insight on what to expect.

If you’ve been on the fence if this would be a good year for you to make a move (buy or sell), give me a call and let’s schedule a consultation. I would love to help.

Holy Shift, Again!

Markets change fast! We experienced a substantial shift in 2022 with the first half of the year feeling like a completely different market than the second half of the year. A 3-point increase in interest rate was the main culprit along with inflation and affordability for the 2022 market correction we experienced. A market correction is defined by prices reverting by 10% or more. In January 2022, the median price in Whatcom County started at $550,000 then peaked at $659,000 in June, and ended the year at $590,000 (-10%). In Skagit County, the median price started at $533,000 then peaked at $595,000 in April, and ended the year at $525,000 (-12%). Keep in mind that the December 2022 median price was also up 17% over the January 2021 median price in Whatcom County and up 18% in Skagit County. This illustrates that the correction was only off the peak of spring 2022 not off of the strong equity that was built prior to that intense run-up.

As we find ourselves in mid-Q1 2023 all data points and anecdotal stories are pointing to most of the market correction being behind us and yet again, another shift. Interest rates peaked in November 2022 at just over 7% and have since come down. Experts are predicting rates to find themselves under 6% as we travel through the easing of inflation in 2023. Some neighborhoods may have a little bit more to go, but others are already showing some growth. Each neighborhood is unique and should be analyzed month by month, but at some point in the first half of the year, we will find stability across the board.

As we find ourselves in mid-Q1 2023 all data points and anecdotal stories are pointing to most of the market correction being behind us and yet again, another shift. Interest rates peaked in November 2022 at just over 7% and have since come down. Experts are predicting rates to find themselves under 6% as we travel through the easing of inflation in 2023. Some neighborhoods may have a little bit more to go, but others are already showing some growth. Each neighborhood is unique and should be analyzed month by month, but at some point in the first half of the year, we will find stability across the board.

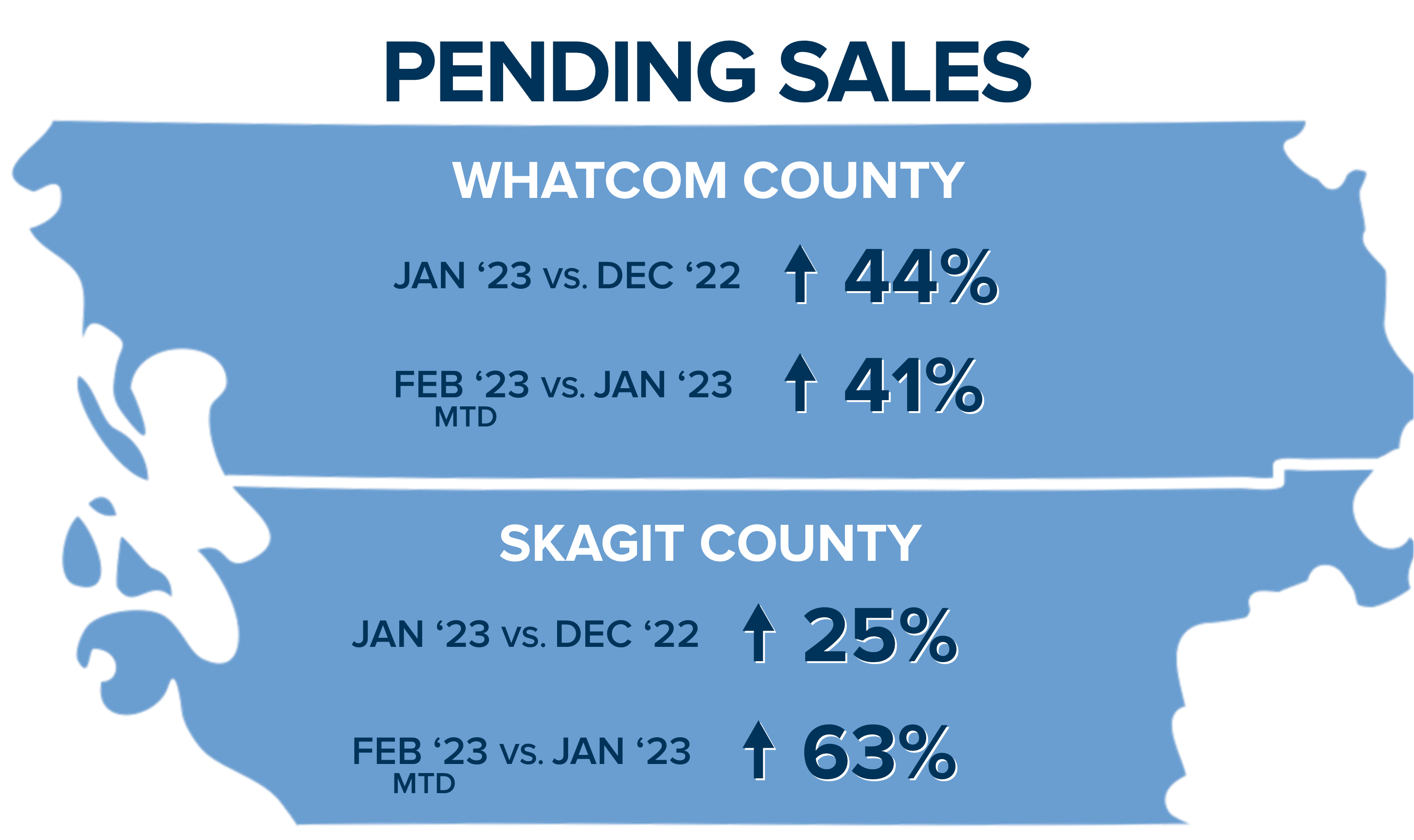

The well-defined price correction and interest rates lowering have brought many buyers back to the market. In fact, pending sales in Whatcom County in January 2023 were up 44% over December 2022. Even more so an indicator: pending sales are up 41% month-to-date (MTD) in February over January 2023! In Skagit County, pending sales in January 2023 were up 25% over December 2022, and up 63% MTD over January 2023.

The well-defined price correction and interest rates lowering have brought many buyers back to the market. In fact, pending sales in Whatcom County in January 2023 were up 44% over December 2022. Even more so an indicator: pending sales are up 41% month-to-date (MTD) in February over January 2023! In Skagit County, pending sales in January 2023 were up 25% over December 2022, and up 63% MTD over January 2023.

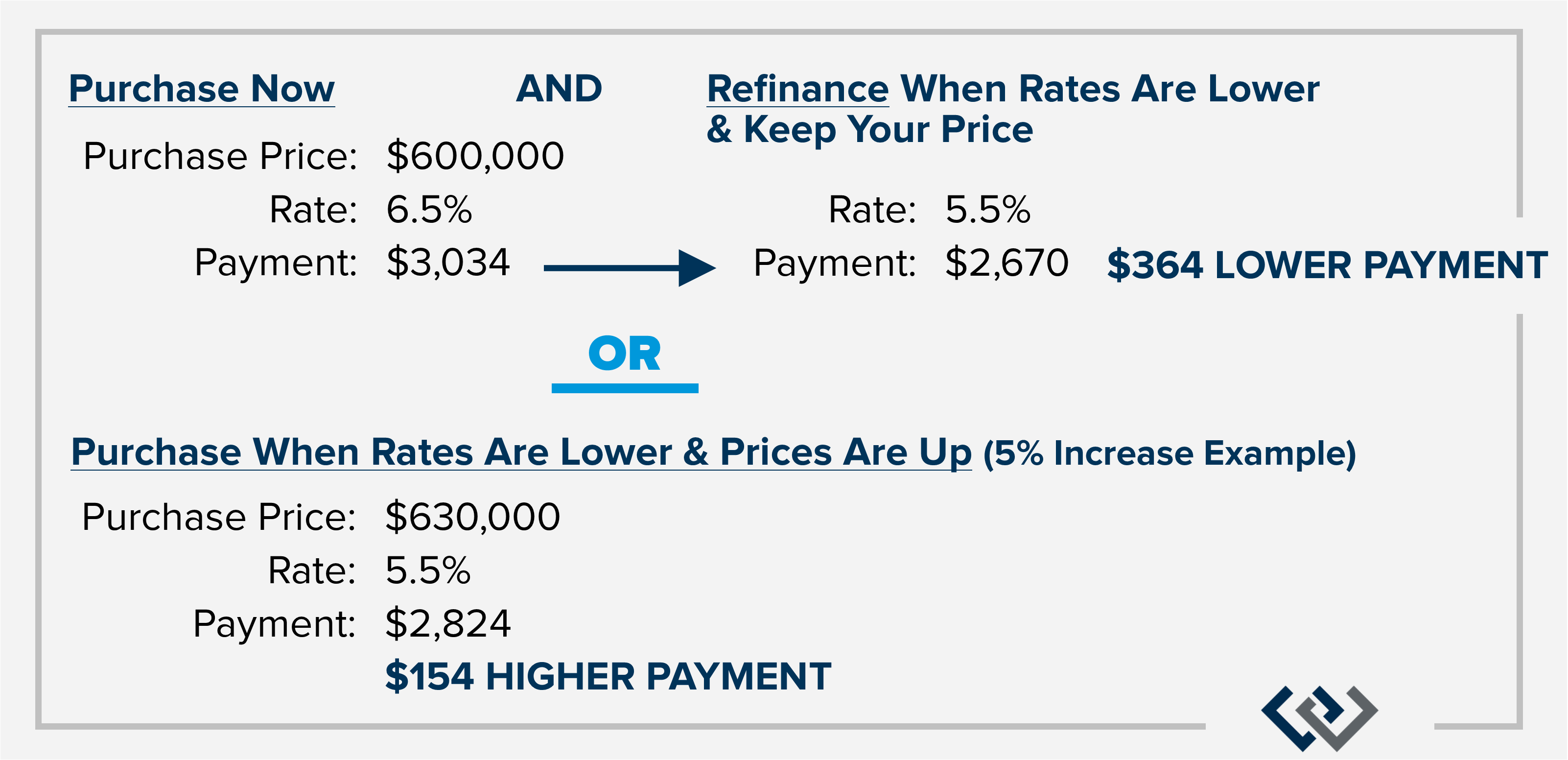

This pent-up demand has come at a time when listing inventory is seasonally scarce and has started to point to an upcoming seller’s market in many areas. Months of inventory is how we define market conditions. 0-2 months is a seller’s market, 2-4 months a balanced market, and 4 months plus a buyer’s market. In Whatcom County, we ended 2022 with 4.4 months of inventory based on pending sales, and in January 2023 had 2.4 months, and MTD is sitting at 2.2 months. In Skagit County, we ended 2022 with 3.2 months of inventory based on pending sales, and in January 2023 had 2 months, and MTD is sitting at 1.3 months.After months of price reductions and searching for the bottom, we are now starting to come across some multiple offers and price increases. This is leaving clues that the bottom was reached and that we are now stabilizing and looking toward the predicted growth that 2023 has to offer. Buyers are eager for additional selection and will welcome the spring influx of new listings. If sellers are ready, they should not hesitate. Should rates lower as the new listings arrive, sellers will be well supported by a willing buyer audience ready to absorb any growth in inventory.Buyers need to understand that rates and prices are closely related and that waiting for rates to hit a certain point may be detrimental to securing a stabilized price. Many buyers are heading into today’s market with a refinance in mind down the road. They are aware that prices will rise as rates lower, so they are looking to obtain a lower price now with a higher rate and once the rate hits their desired level, they will refinance to lower their payment all while holding on to their lower basis point.For example, if a buyer bought now at $600,000 with 20% down and a rate of 6.5% their monthly principal and interest payment would be $3,034. If a year from now, rates are at 5.5% and prices are up 5% and that same buyer refinances, they will save $292 a month on their payment and $30,000 in principal. This would also be $154 lower than what the payment would be at the appreciated price with the lower rate!

|

|

|

New Park Along Bellingham Waterfront

Plans that began in 2014 are finally moving quickly for this new Bellingham park. Salish Landing is the name chosen for the 17 acres at the south end of Cornwall Ave along Bellingham Bay toward Boulevard Park. Permit application for cleanup and work is now pending as the city focuses on cleaning up the decades of pollution in the area from the city dump and multiple industry operations in the area. There is not an expected opening date yet, but once development is complete, this park will have beach access, trails, parking, restrooms, benches, bike racks, and a kayak launching and landing site. I am excited to check out this new park and all it will have to offer!

I’m hopeful it will come together quickly, but we all know the pace at which projects like this come together… any guesses on how long it will take to open?!

Why We Love Living In Whatcom County

I recently asked some of my clients why they love living in Whatcom County. There are some strong similar storylines no matter whom you ask! Here are a few of the answers…

The Lifetime Resident

Q. What makes Whatcom County a great place to work and live?

A. “Even though our city keeps growing, it still feels small. I love that anywhere I go I’m going to know someone. But my favorite thing really is the proximity to the water and the mountains. The beer culture is unrivaled and even though I’m an avid traveler I always feel like there’s something new to discover in my home town.”

The Relocated Retiree

Q. Why would you recommend Whatcom County for someone looking to move here?

A. “I love the the beauty and weather in this area. There is so much outdoor beauty, it’s not overdeveloped, and there is enough water for the future!”

The New Family in Town

Q. What is your favorite thing about living in Whatcom County?

A. “The best part of living in Whatcom County is being surrounded by mountains on one side, and water on the other side. There is a strong sense of community. Bellingham’s location makes it easy to be active outdoors.”

National Market Summary

|

|

|

Across the nation, we saw a real estate market correction in 2022 as interest rates doubled. Interest rates started the year at just over 3%, peaked in November at just over 7%, and ended at just under 6.5%. Since the first of the year, we are closer to 6% and anticipate rates to continue to improve towards 5% throughout 2023. The Feds utilized rising interest rates to combat inflation in an effort to create a short recession to slow the cost of all products and services after record-breaking increases during the pandemic. This has reduced spending due to money becoming more expensive to borrow and corrected prices across many industries, including housing.

Across the nation, we saw a real estate market correction in 2022 as interest rates doubled. Interest rates started the year at just over 3%, peaked in November at just over 7%, and ended at just under 6.5%. Since the first of the year, we are closer to 6% and anticipate rates to continue to improve towards 5% throughout 2023. The Feds utilized rising interest rates to combat inflation in an effort to create a short recession to slow the cost of all products and services after record-breaking increases during the pandemic. This has reduced spending due to money becoming more expensive to borrow and corrected prices across many industries, including housing.

|

|

The worst of this correction seems to be behind us as rates are expected to continue to improve throughout 2023 and consumers are adjusting to a more normalized market. Prices are starting to stabilize and are near, if not at the bottom, and should have modest growth in the second half of 2023. We are already starting to see pending sales pick up. Month-to-date (MTD), pending sales are up 36% in Whatcom County over December (month-over-month, MOM). This increase in pending sales is coupled with available inventory being down 15% MOM in Whatcom County. In Skagit County pending sales are down MOM, but by only 8% while available inventory is down by 16%. Inventory remains tight with MTD inventory levels shifting from a balanced market to a moderate seller’s market based on pending sales rates in both counties.

The worst of this correction seems to be behind us as rates are expected to continue to improve throughout 2023 and consumers are adjusting to a more normalized market. Prices are starting to stabilize and are near, if not at the bottom, and should have modest growth in the second half of 2023. We are already starting to see pending sales pick up. Month-to-date (MTD), pending sales are up 36% in Whatcom County over December (month-over-month, MOM). This increase in pending sales is coupled with available inventory being down 15% MOM in Whatcom County. In Skagit County pending sales are down MOM, but by only 8% while available inventory is down by 16%. Inventory remains tight with MTD inventory levels shifting from a balanced market to a moderate seller’s market based on pending sales rates in both counties.

|

Home Fresh 2022 Update

6 years ago I made a commitment to serve my community with a donation of 1,000 pounds of fresh produce for every purchase or sale. This year, you helped me donate 31,000 lbs. This means that over the past 6 years you have helped donate over 202,000 lbs! Every time you send a friend or family my name you are helping me build my business and helping me give back even more! Thank you friends!

2022 Recap

2022 can’t be summarized with just a slideshow of properties sold- it was SOOO MUCH more than that. So much more than any other year because it was the year business finally felt genuine.

Yes, I helped 40 families achieve their goals in real estate. We celebrated with joy and cried tears of frustration and sadness together. That’s just incredible on its own but I also found my partner in crime – the person I always needed to get all the OTHER stuff done! Together with Heather Maddox we made huge strides in pushing our industry to show up in a way that feels so good! We’ve fostered collaboration and authentic connection through Collaboration over Competition – all the photos you see between the homes I sold are evidence of collaboration‼️

Heather and I hosted 4 Supper Clubs, taught courses for Windermere , hosted monthly lunches in own own markets, were main stage speakers at Genuine Hustle across the country AND hosted almost 40 guests on our weekly Instagram Live Show.

I added two incredible ladies to my team to support me, my clients and this passion project- Looking back on it all I’m not sure how we accomplished so much. But I also can’t imagine how I felt complete in prior years without it all!

Thank you to all of you who contributed- clients, friends, friends who send your friends my name, fellow brokers. 2022 was the best year ever, and I’m looking forward to so much more in 2023!

Key Factors to Note as the Market Recalibrates in the New Year

2022 has been an eventful year in the real estate market and the economy. After 2 years of pandemic-fueled demand and historically low interest rates, we experienced a shift. The Fed quickly raised rates (by 2 points) from April to October to combat inflation, curbing buyer demand as affordability took a hit. The overall economy is starting to settle back to pre-pandemic levels and the second half of 2022 was the time that was needed to make this adjustment.We have recently seen rates drop as year-over-year inflation numbers start to show improvement. We anticipate this trend to continue slowly but surely as we head into 2023 and beyond. The upward trend in rates has put downward pressure on prices, but they are starting to stabilize as the new normal sets in. Price appreciation is still up year-over-year when you look at the average of the last 12 months and compare them to the previous 12 months, and certainly over the last 3-10 years as a whole.We started 2022 at 3.5%, peaked at just over 7%, and now find rates in the low to mid-6%. Experts like Matthew Gardner are anticipating rates to settle in the high 5% sometime in 2023, which would be 2 points below the historical average. Currently, buyers are enjoying more favorable negotiations and are securing sale prices that are not escalating at a feverish pitch.Some buyers are getting creative and using seller credits for a rate buy-down, some are securing adjustable-rate mortgages, and some just plan to re-finance when rates come down further next year. It is important for buyers to understand that as rates come down prices will start to fortify again. Besides rates and prices, which are related, two additional factors to pay attention to are our local job market and estimating the recession. We have recently experienced some layoffs in our region, particularly in the tech sector. See the video from Matthew Gardner here which speaks to this. The bottom line is over 20,000 jobs were added in the information sector during the pandemic, and that number is now receding. Just like prices grew exponentially during the pandemic, so did many other aspects of the economy and everything is finding its equilibrium as we return to our new normal. Bear in mind, there are other sectors of our local job market that are growing.I’d like to leave you with two pieces of advice as we head into 2023 and are forced to jump on the media roller coaster of their reporting economic and real estate news. Pay attention to long-term figures and understand that real estate is a lifestyle move, not just a financial chess move.The media will paint the picture that the sky is falling and it simply is not. The recession is predicted to be short, much like the recession of 1990-91. Some economists are claiming that we are already through the worst of it. This will be nothing like the Great Recession of 2007-2012, nothing! It just happens to be the one closest in our rear-view mirror and easiest to recall, but that was made up of entirely different factors that do not compare to our current environment. Please reach out if you’d like to further discuss the differences.We are not headed toward a bubble in the real estate market. Homeowner equity is incredibly strong with over 50% of all homeowners in WA state having over 50% home equity. Homes are not foreclosed on when there is equity—period, end of story. As numbers are reported in the first half of 2023 they will be compared to the peak prices of 2022 and those numbers will create negative headlines. We will spend the first half of 2023 adjusting off of those peaks, but where I am sure the media will fall short is reporting the overall growth in values since 2019.Real estate is a long-term hold investment, it always has been. The ramp-up of the pandemic years may have clouded that long-term truth, but I can assure you double-digit and certainly 20%+ annual appreciation is not normal. The historical norm is 3-5% annually. For example, in Whatcom County when you take the last 12 months of median price and average it and compare it to the previous 12 months, prices are up 12%. When you take the median price in Nov 2022 and compare it to the median price in Nov 2021, prices are down 3%. Further, when you take the median price in Nov 2022 and compare it to the median price two years ago in Nov 2020, prices are up 23%. We are experiencing a correction off of the peak, not a tumbling of long-term values. Hence, why there is no bubble.In fact, experts are anticipating that we end 2023 with positive, yet slight year-over-year appreciation. This is more reflective of historical norms and much calmer than the intense pandemic-fueled years that were inflated with rates that we will quite possibly never see again in our lifetime.Lastly and most importantly, real estate moves are most often motivated by life changes. Job changes, familial changes, and financial shifts lead to people changing their housing and location. These big life changes are delicate and exciting, and require strategic planning and care. I am all about helping my clients obtain successful financial results, but I am also committed to helping my clients navigate the details, challenges, emotions, and logistics of a move. I always approach the process with the end in mind, but also with the journey prioritized to be smooth and enjoyable.I hope you call on me when your curiosity is piqued or you have an emergent need in your world related to real estate. I take pride in understanding the latest trends and helping you apply them to your goals. Also, if you know of anyone that needs real estate help, please pass my name along or get me in touch with them. Your people are my people, and helping them stay well-informed to empower strong decisions is my mission. As we encounter change and recalibrate, this expertise will be more important than ever; I am honored to have your trust and endorsement.

Besides rates and prices, which are related, two additional factors to pay attention to are our local job market and estimating the recession. We have recently experienced some layoffs in our region, particularly in the tech sector. See the video from Matthew Gardner here which speaks to this. The bottom line is over 20,000 jobs were added in the information sector during the pandemic, and that number is now receding. Just like prices grew exponentially during the pandemic, so did many other aspects of the economy and everything is finding its equilibrium as we return to our new normal. Bear in mind, there are other sectors of our local job market that are growing.I’d like to leave you with two pieces of advice as we head into 2023 and are forced to jump on the media roller coaster of their reporting economic and real estate news. Pay attention to long-term figures and understand that real estate is a lifestyle move, not just a financial chess move.The media will paint the picture that the sky is falling and it simply is not. The recession is predicted to be short, much like the recession of 1990-91. Some economists are claiming that we are already through the worst of it. This will be nothing like the Great Recession of 2007-2012, nothing! It just happens to be the one closest in our rear-view mirror and easiest to recall, but that was made up of entirely different factors that do not compare to our current environment. Please reach out if you’d like to further discuss the differences.We are not headed toward a bubble in the real estate market. Homeowner equity is incredibly strong with over 50% of all homeowners in WA state having over 50% home equity. Homes are not foreclosed on when there is equity—period, end of story. As numbers are reported in the first half of 2023 they will be compared to the peak prices of 2022 and those numbers will create negative headlines. We will spend the first half of 2023 adjusting off of those peaks, but where I am sure the media will fall short is reporting the overall growth in values since 2019.Real estate is a long-term hold investment, it always has been. The ramp-up of the pandemic years may have clouded that long-term truth, but I can assure you double-digit and certainly 20%+ annual appreciation is not normal. The historical norm is 3-5% annually. For example, in Whatcom County when you take the last 12 months of median price and average it and compare it to the previous 12 months, prices are up 12%. When you take the median price in Nov 2022 and compare it to the median price in Nov 2021, prices are down 3%. Further, when you take the median price in Nov 2022 and compare it to the median price two years ago in Nov 2020, prices are up 23%. We are experiencing a correction off of the peak, not a tumbling of long-term values. Hence, why there is no bubble.In fact, experts are anticipating that we end 2023 with positive, yet slight year-over-year appreciation. This is more reflective of historical norms and much calmer than the intense pandemic-fueled years that were inflated with rates that we will quite possibly never see again in our lifetime.Lastly and most importantly, real estate moves are most often motivated by life changes. Job changes, familial changes, and financial shifts lead to people changing their housing and location. These big life changes are delicate and exciting, and require strategic planning and care. I am all about helping my clients obtain successful financial results, but I am also committed to helping my clients navigate the details, challenges, emotions, and logistics of a move. I always approach the process with the end in mind, but also with the journey prioritized to be smooth and enjoyable.I hope you call on me when your curiosity is piqued or you have an emergent need in your world related to real estate. I take pride in understanding the latest trends and helping you apply them to your goals. Also, if you know of anyone that needs real estate help, please pass my name along or get me in touch with them. Your people are my people, and helping them stay well-informed to empower strong decisions is my mission. As we encounter change and recalibrate, this expertise will be more important than ever; I am honored to have your trust and endorsement.