Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Gov. Inslee’s Wa Recovery Plan

|

|

|

Current Numbers that Matter – Week 6

|

Current Numbers that Matter – Week 5

|

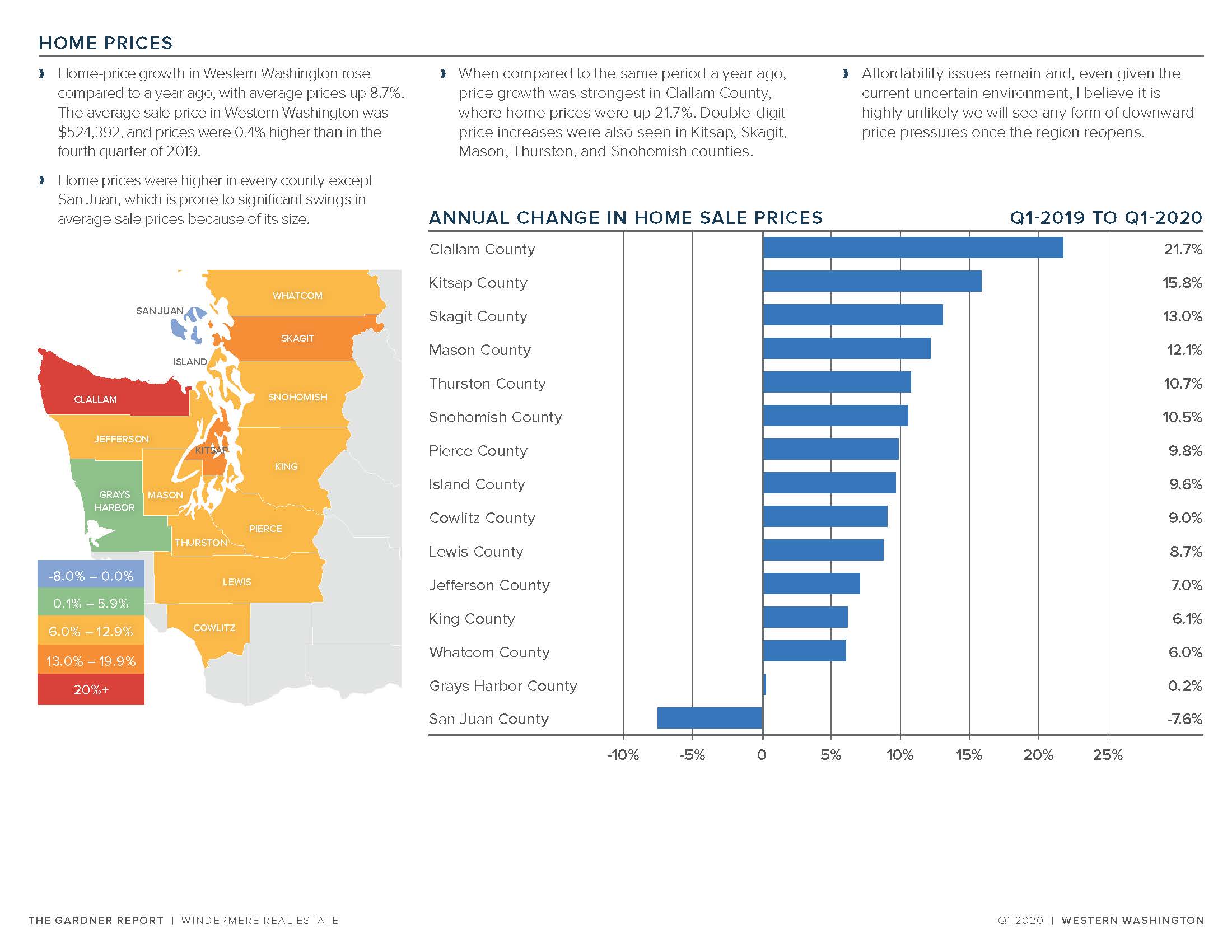

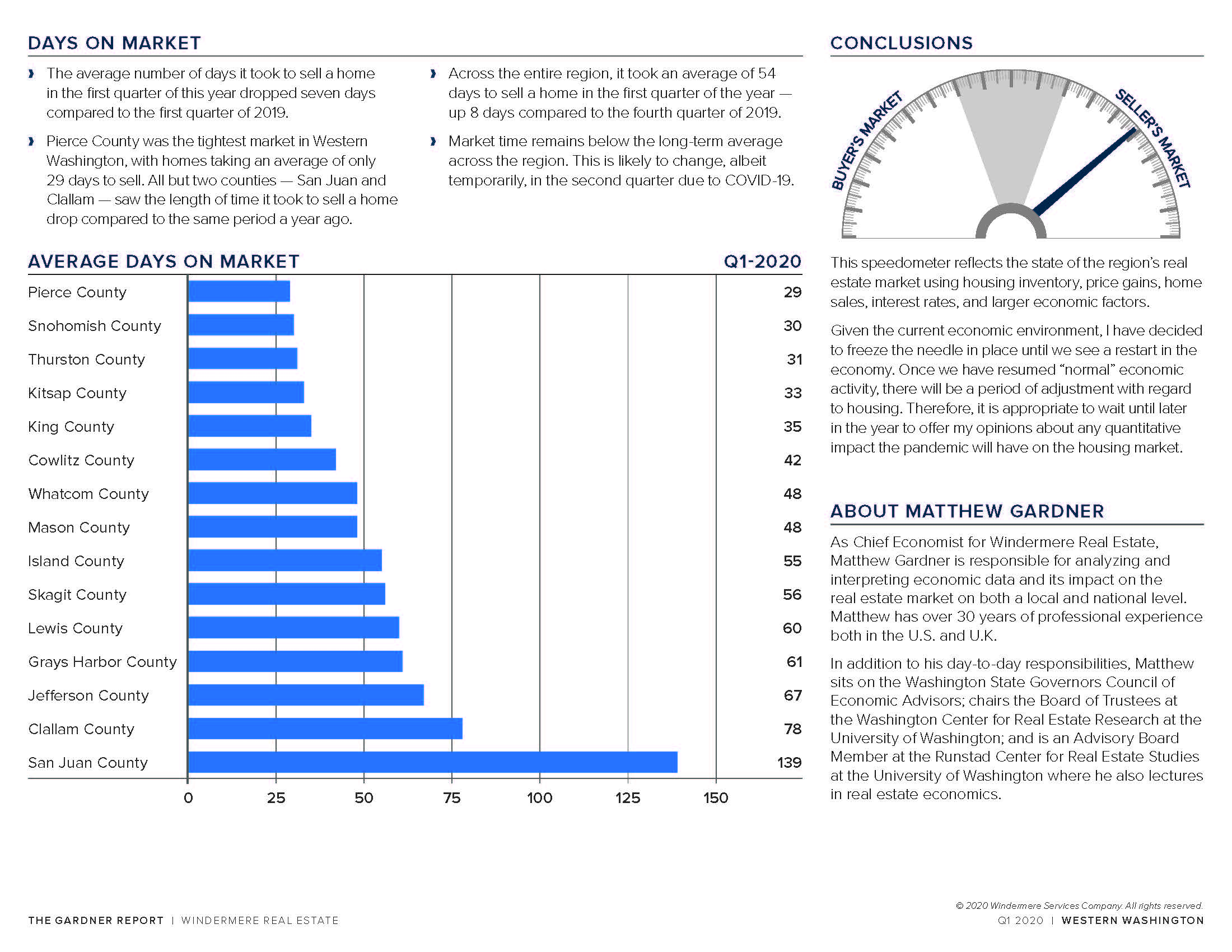

Q1 2020 { Western Washington Gardner Report }

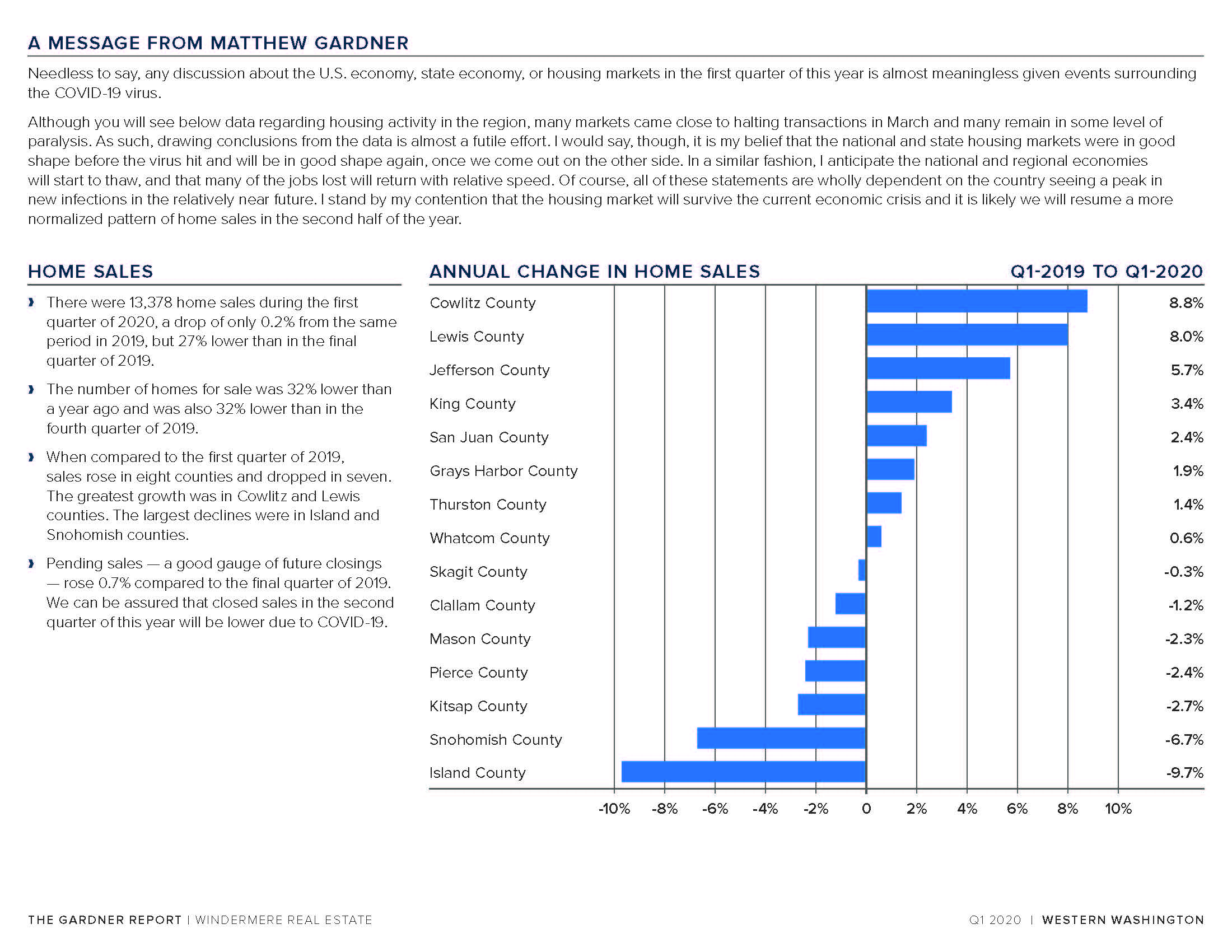

A Message from Matthew:

Needless to say, any discussion about the U.S. economy, state economy, or housing markets in the first quarter of this year is almost meaningless given events surrounding the COVID-19 virus.

Although you will see this data regarding housing activity in the region, many markets came close to halting transactions in March and many remain in some level of paralysis. As such, drawing conclusions from the data is almost a futile effort. I would say, though, it is my belief that the national and state housing markets were in good shape before the virus hit and will be in good shape again, once we come out on the other side. In a similar fashion, I anticipate the national and regional economies will start to thaw, and that many of the jobs lost will return with relative speed. Of course, all of these statements are wholly dependent on the country seeing a peak in new infections in the relatively near future. I stand by my contention that the housing market will survive the current economic crisis and it is likely we will resume a more normalized pattern of home sales in the second half of the year.

As always, if you have any questions or want to chat about what this information means for you, please give me a call (360-201-6433) or send me an email : Tracieg@windermere.com.

LENDING UPDATE W/ LENA

|

|

|

Tax Updates

The IRS issued guidance Thursday evening to grant deadline relief for both 1031 like-kind exchanges and opportunity zone investments that are already underway. Both of these programs are designed to promote economic growth in communities, and the National Association of Realtors made the case that investors in these programs should not be harmed due to the effects of COVID-19.

- 1031 Like-kind exchanges. If an investor has taken the first step of a like-kind exchange by selling the old property, and either the 45-day or the 180-day deadline falls between April 1 and July 15, the deadline has been extended to July 15.

- Opportunity Zones. If an investor who sold a capital asset planned to roll over the gain into an Opportunity Fund and the 180-day deadline to do so falls between April 1 and July 15, 2020, he or she can make the investment as late as July 15.

Also, sole proprietors who pay quarterly estimated taxes now have until July 15 to file their second quarter payment. As a result of an earlier IRS notice, first quarter estimated tax payments had already been extended to July 15. This means that any individual or corporation that has a quarterly estimated tax payment due on or after April 1, 2020, and before July 15, 2020, can wait until July 15 to make that payment, without penalty.

NAR has advocated heavily for these extensions since the outbreak of the COVID-19 pandemic. We’ll have a full analysis of this announcement Friday on our dedicated coronavirus page.

Current Numbers that Matter – Week 4

Data, Tours, Taxes and Interest Rates

Most prominent in the news this last week was Washington State deciding that our students will not return to in person schooling this school year. Families are mourning sadness of missing out on the end of year celebrations for milestone grade transitions, cancelled sports seasons and so much more. I’m with you all experiencing some of this sadness and if there is any way I can support you or help you celebrate something, please let me know!

This is week 4 of analyzing data in Whatcom County to observe the affects of COVID-19 on our housing market.

BACK TO THE DATA

Numbers seem to be going up! Whatcom County total homes that went Active this week rose from 52 to 95, which is a pretty big jump in one week considering our current situation! There is now only a difference of 21 homes from last year to this year.

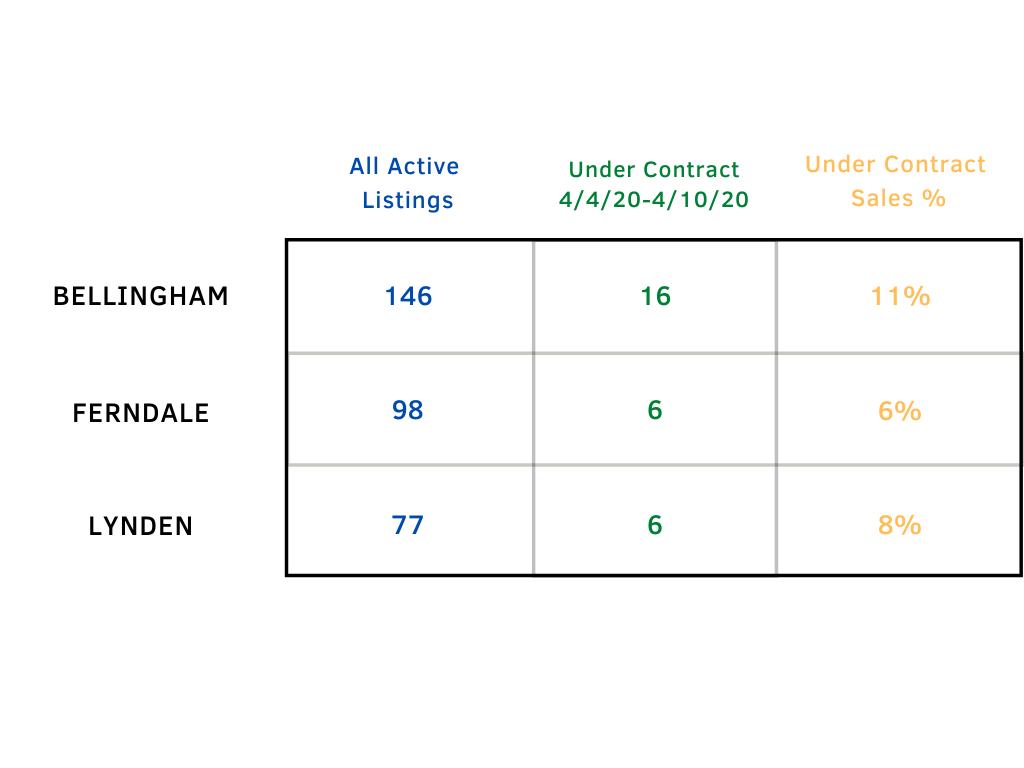

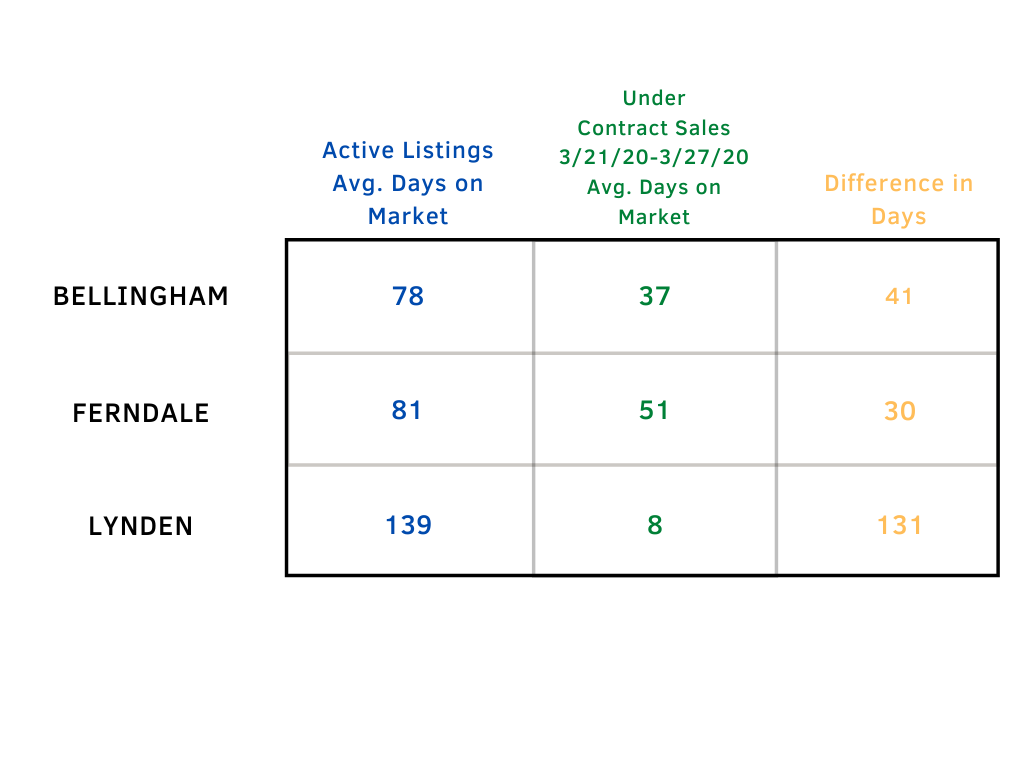

UNDER CONTRACT

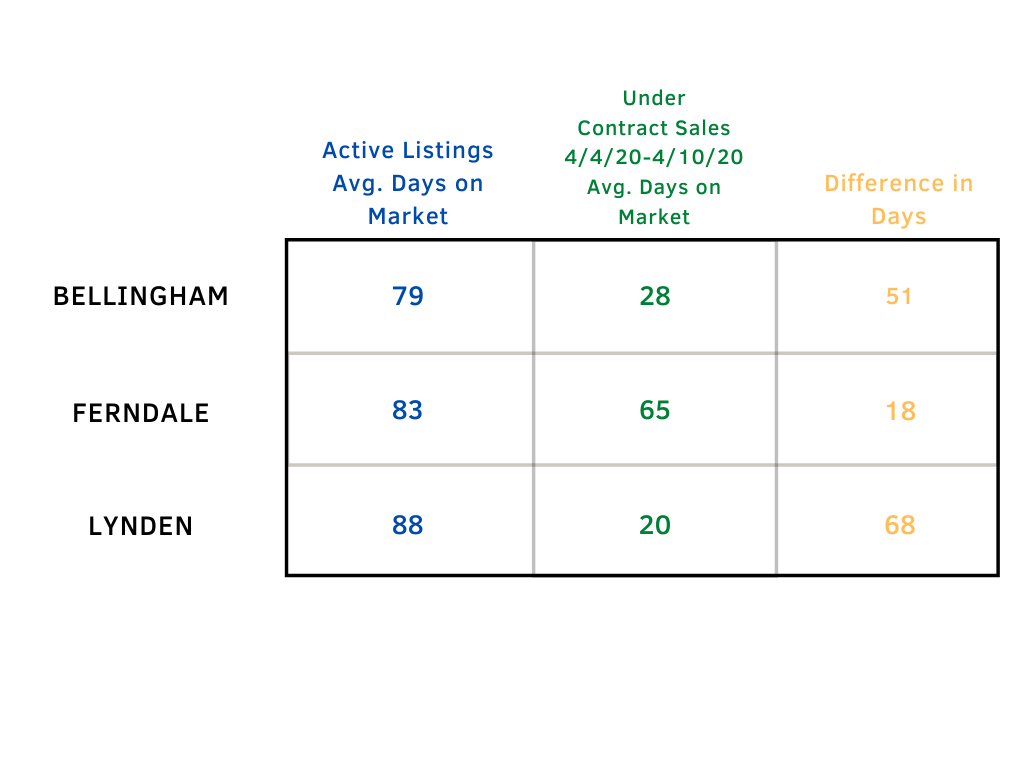

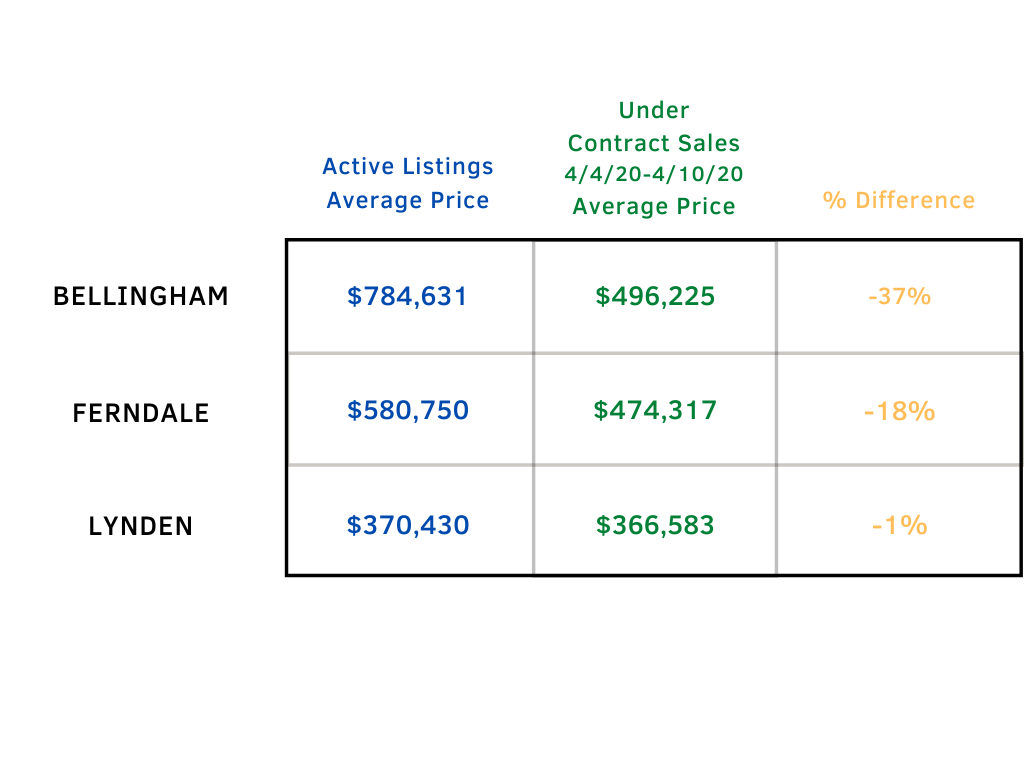

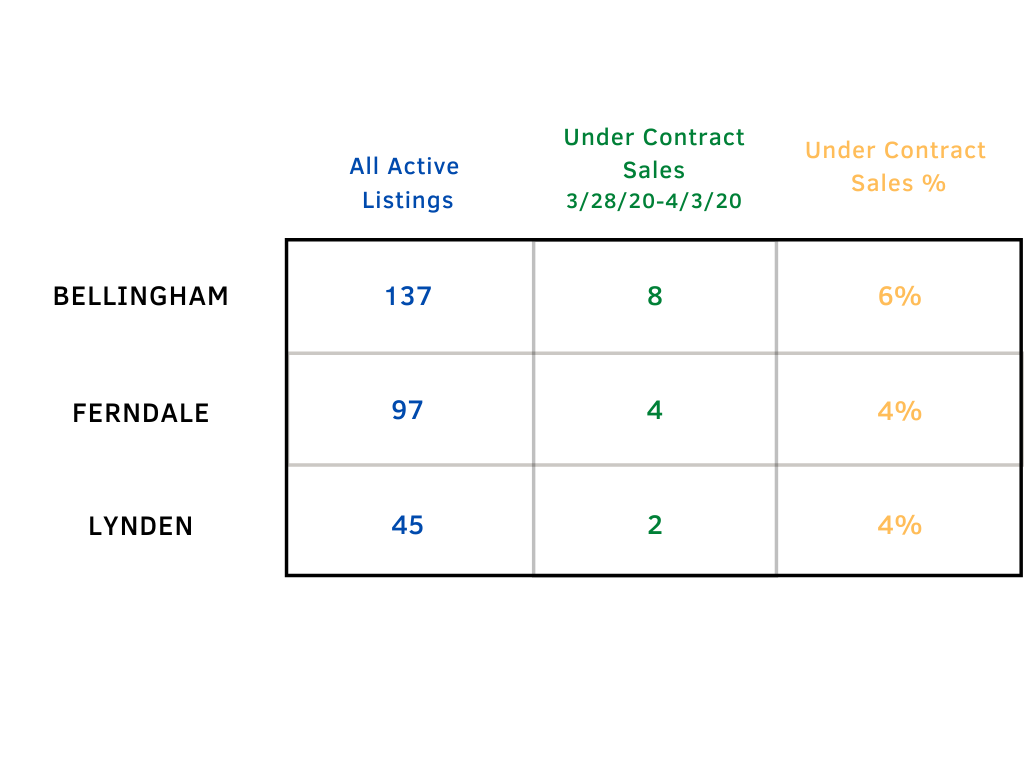

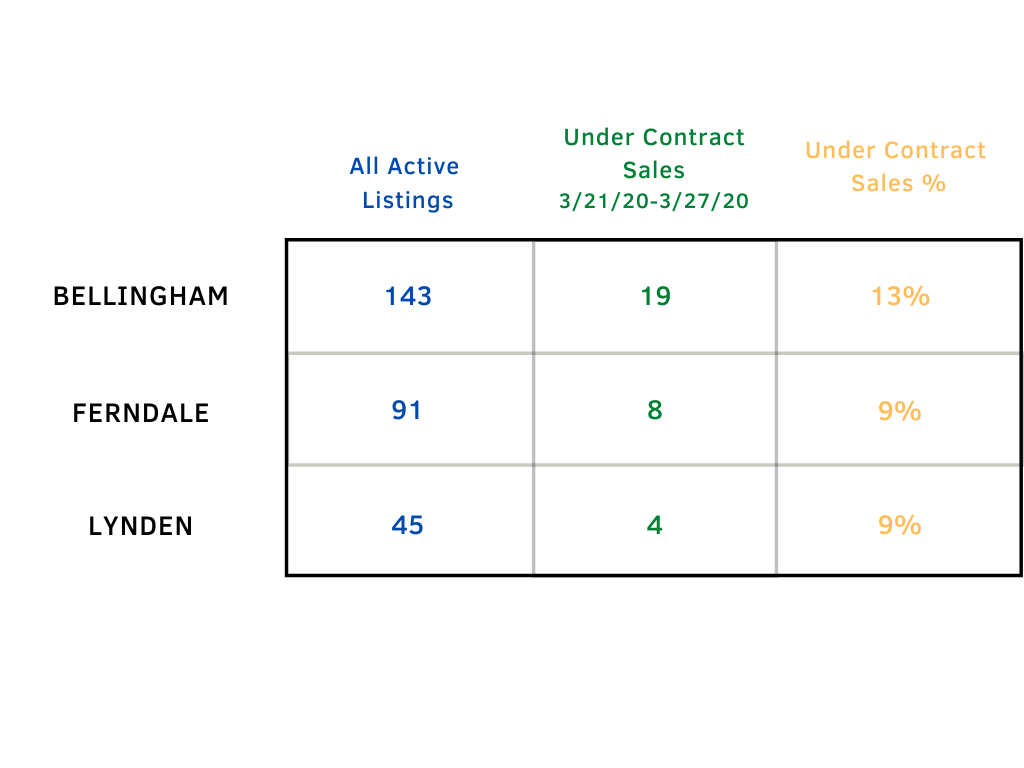

Below is an accounting of all of the active listings on the market in our three major markets along with all of the sales that went under contract from 4/4/20 to 4/10/20 (pulled around Noon PST) and the percentage relationship between those numbers.

Remember when Real Estate wasn’t deemed an “Essential Business,” and numbers went down? Well, look what happens when we are “Essential” again! Please know that we are all taking great caution and limiting exposure to families by only taking clients into others homes that have urgent housing needs. Pendings are back up! The Under Contract numbers for Bellingham doubled since last week, and Lynden has 32 new active listings!

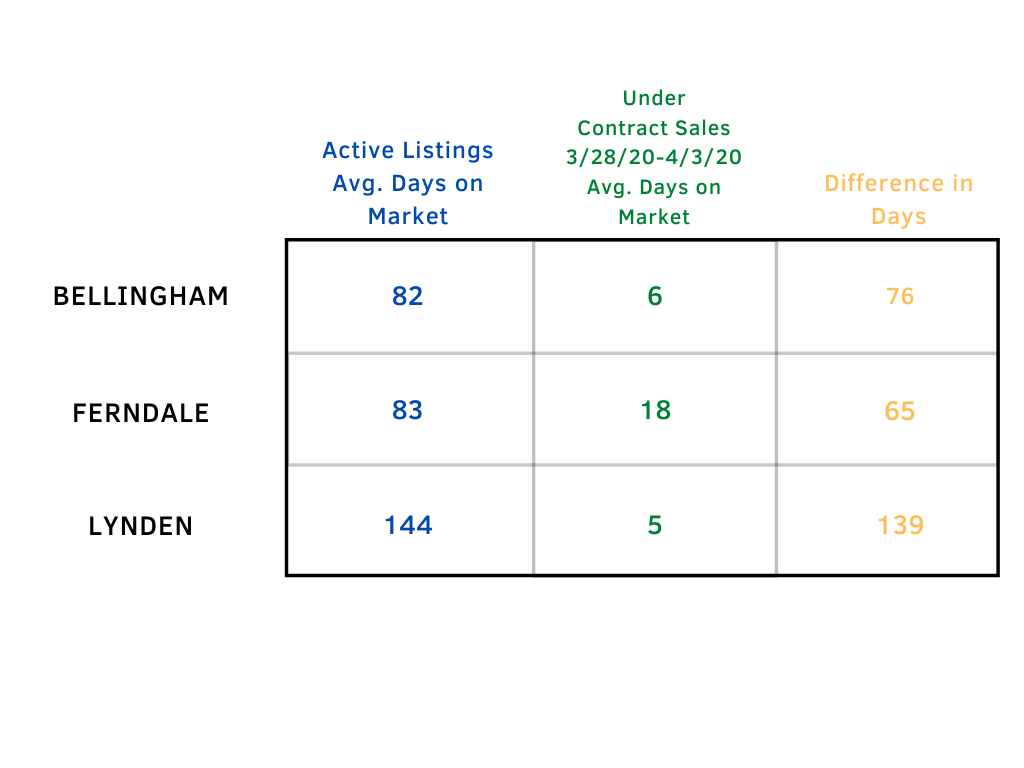

ADOM

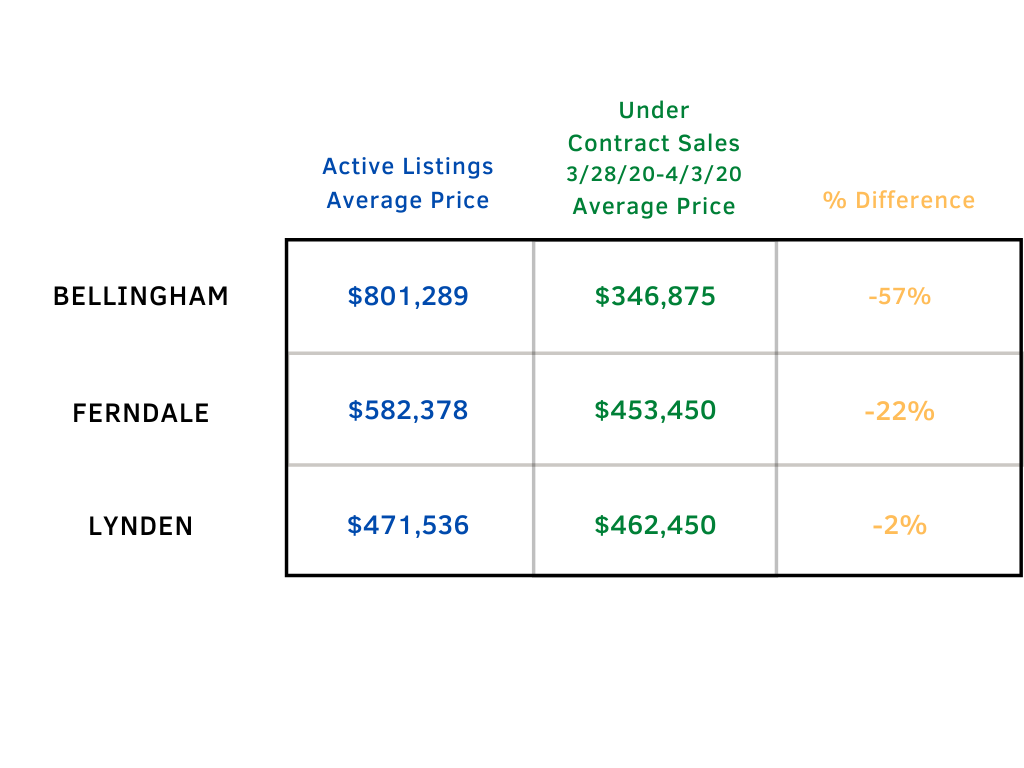

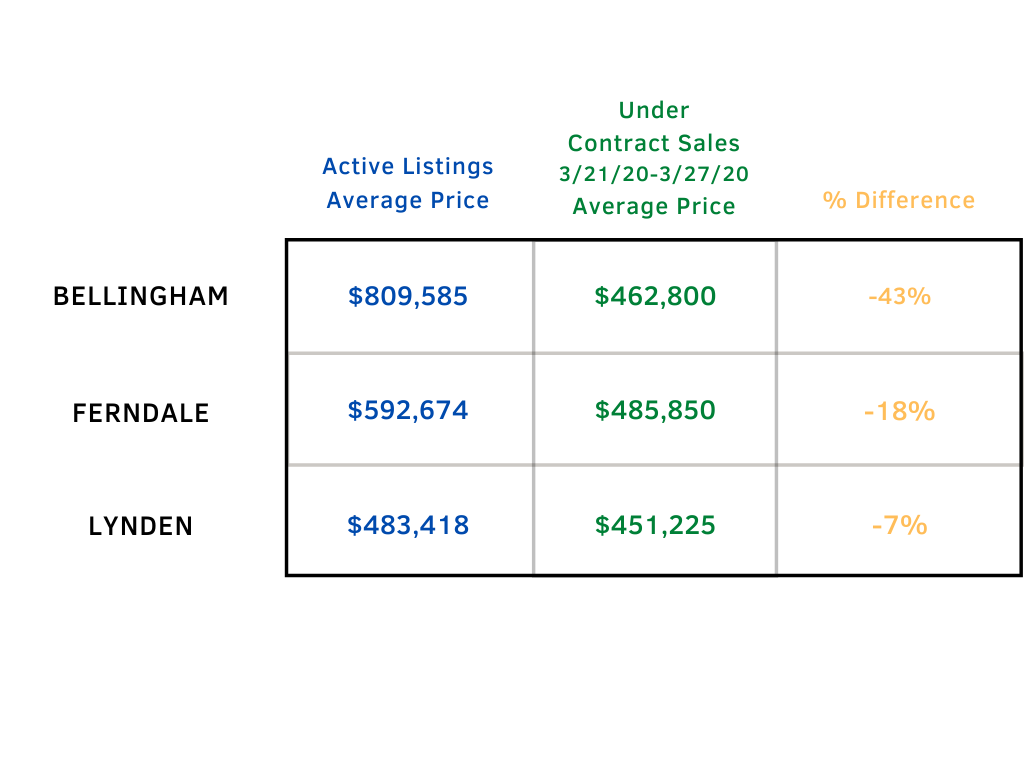

% PRICE DIFFERENCE

Current Numbers that Matter – Week 3

May the 4th Be… Here Quickly!

Here we are again with another update on our Stay at Home Directive, which now has been extended until May 4th. It might seem like so far away, but the more we stay home (and the better we follow the rules), the sooner we will be able to resume our regular lifestyles!

I’m continuing with week 3 of looking at specific data from Bellingham, Ferndale and Lynden to observe the affects COVID-19 has on the current housing trends. You’ll find the updated charts below and my comments regarding them. However, before we get into the nitty gritty, watch the video below for some good news!

BACK TO THE DATA

As we are in an ever-changing climate (it seems day-to-day), I want to reiterate that the BEST time to list a home for sale, I believe, will be 1 week after the Stay Home Directive is lifted. As Economist Matthew Gardner has stated in his Monday Update this week, “We are currently in a Health Crisis, NOT a Housing Crisis.” Most things in our life right now, unless they were already in process or are essential, have been put on hold. When we are able to get back to “normal life” that will all start back up again. New listings will go active, and buyers will be ready as ever to find a new home! As I projected last week, the numbers have dwindled slightly, but not significantly as you’ll see below.

UNDER CONTRACT

ADOM

% PRICE DIFFERENCE

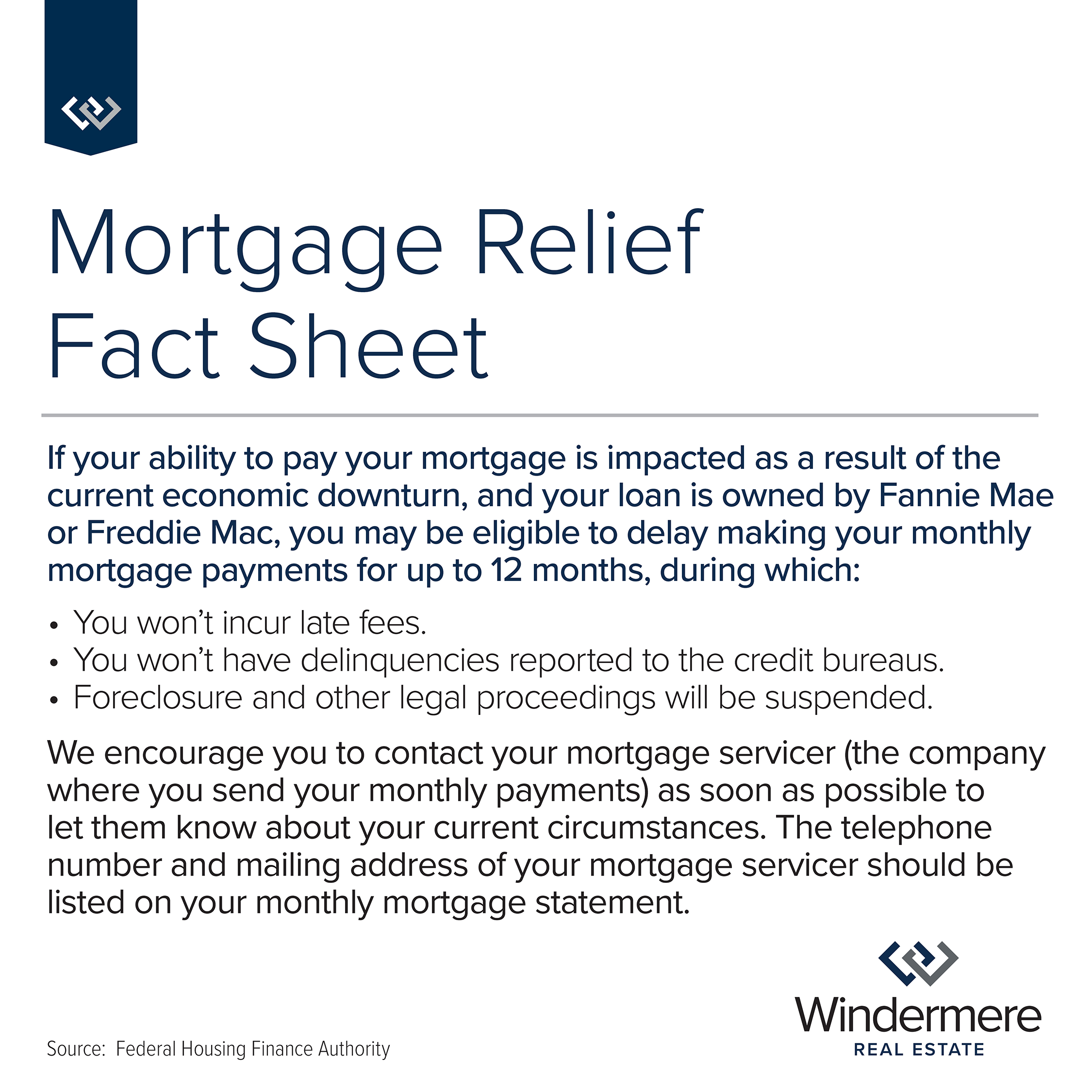

MORTGAGE RELIEF

A MAJOR aspect that is different from the recession we are heading into and the 2008 Great Recession is that some banks and mortgage investors (servicers) are working with homeowners to provide mortgage relief. With the shutdown of so many businesses and services, job losses (hopefully they are temporary) have been abundant.

If you or someone you know would benefit from setting up a mortgage forbearance program or loan modification in order to alleviate the pressure of monthly payments right now, click on this link and have them contact their mortgage servicer today. The available programs that are offered will vary from one loan servicer to another, and are primarily available for loans that are owned by Fannie Mae or Freddie Mac (click on the appropriate link to help research who owns your loan).

Make sure you consider the details and payback terms for your long-term financial health. Your ability to protect your largest asset (your home) while waiting this out will protect your equity! This is a milestone opportunity and will ensure a strong housing market moving forward.

SMALL BUSINESS HELP

We care about local small business and want to be able to help you thrive in any way we can! If you own a small business like I do, chances are this health crisis we are in has had an effect on your stress levels. Well, this information graciously provided by my tax advisor should help!

Recently, Congress passed the CARES Act (Coronavirus Aid, Relief and Economic Security). This is designed to assist small businesses steadily throughout the VOVID-19 crisis and provide the ability to keep their employees. There are two major parts to the act: The Small Business Administration Emergency Injury Disaster Loans, administered by the SBA, and the Paycheck Protection Program, administered by private banks. Down below, I have included an infographic about applying for a Paycheck Protection Program loan, which can be up to 2.5 times your average monthly payroll costs, with the possibility of the loan being forgiven.

Here’s a helpful list of 10 FAQ’s from the US Chamber of Commerce about the loans of the CARES act

1. What loans are available to help small businesses during Coronavirus?

The Economic Injury Disaster Loan from the SBA.

The Payroll Protection Loan.

2. How do I get these loans?

Apply for the Economic Injury Disaster Loan directly from the SBA here.

Payroll Protection Loans are government-backed but will come from private banks. You should inquire at your local bank about these loans.

3. How much can I borrow?

The EIDL from the SBA can be up to $2 million working capital for up to a 30-year term at 3.75% (2.75% for non-profits). Not everyone will qualify for that amount.

The Payroll Protection Loans can be for 2.5 months of average payroll or $10 million, whichever is less [note: employee health care plan costs can be included – see the attachment].

4. Do I need to repay these loans?

The EIDL from the SBA will be repaid. Payments can be deferred for one year after the origin of the loan.

All or some of the Payroll Protection Loan may be forgiven (converted into a grant). There are specific requirements about how you spend the loan and if you continue to employ your workers in order for it to be forgiven.

5. What about the $10,000 emergency grant I’ve heard about?

The SBA is offering to advance businesses a $10,000 grant that does not need to be paid back. That grant can be paid quickly – in as little as three days.

You can apply for that $10,000 grant as part of the EIDL process. If you are awarded the $10,000 emergency grant, you will not have to pay the grant amount back. You will still have to repay the rest of your SBA EIDL.

6. Can self-employed and freelancers apply?

Paycheck Protection Loans are available to 501(c)(3)s, self-employed, sole proprietors and independent contractors.

SBA EIDLs are available to small businesses and non-profits (including faith-based) with fewer than 500 employees, sole proprietors and independent contractors.

7. Can I apply for both loans?

Yes. You can apply for and receive both loans.

8. Do I need good credit to qualify for these loans?

The Payroll Protection Loan requires no collateral and no personal guarantee.

The EIDLs are given based on credit scores. No tax returns are required. You can borrow up to $200,000 without a personal guarantee.

9. What if I’ve already fired or laid off my employees? Do I still qualify for a Payroll Protection Loan?

Your loan may be forgiven if you bring back employees and restore wages generally within 30 days and maintain them through June 30.

10. My bank doesn’t seem to know anything about the Payroll Protection Loan. Now what?

Banks are currently working out the details. If your bank hasn’t heard about the loan yet, try a bank that is already an approved SBA lender [note: in the Bellingham area, these include Umpqua Bank, Wells Fargo, Chase, US Bank, KeyBank, and Bank of America]. They may be more familiar with the process.

For help in navigating the loan process and other aspects of this crisis, SCORE, a well-established small business mentoring program, is available to do remote mentoring. In addition, they will be conducting webinars and online workshops for dealing with the fallout from Coronavirus and the help available. You can learn more here.

| Please contact me with your questions and concerns, I am committed to help keep you informed! Best Wishes! |

REVISED Current Numbers that Matter – Week 2

|

Current Numbers that Matter- Week 2

SO MUCH CHANGE

It is hard to believe our lives could have changed much more in this last week than they did the week before, but it certainly happened, didn’t it?!

Here’s a Timeline of the last week’s significant events for reference:

- Sunday 3/22- President Trump approved our state’s disaster declaration

- Monday 3/23- Boeing suspended production at it’s Puget Sound facilities and Gov. Inslee directed a “Stay at Home Order”

- Tuesday 3/24- Summer Olympics in Tokyo Postponed

- Wednesday 3/25- “Stay at Home” began and all non-essential business closed and the $2 trillion Federal Aid Package was reached

If you are currently planning a move, and are active in the Real Estate Market, you likely heard that Real Estate Brokers (that’s me) are NOT considered essential. What does this mean for you, and my clients? I am only able to continue to advocate for and support my clients from my HOME OFFICE. This means a lot of video conferencing, phone calls and computer work. Homes that are currently under contract (pending) are able to move forward because financial (real estate loans) and government (recording the sale) sectors are able to continue to operate. But for the rest of you, this means we are unable to go see a home or list your home unless we already have it all prepared for market. In fact, the NWMLS is actually issuing fines for any broker who uses their app on their phone to open a key box and access a home!

BACK TO THE DATA

UNDER CONTRACT

ADOM

% PRICE DIFFERENCE

SILVER LINING

I will continue to monitor and stay on top of these changes for you, so we can continue to plan for your Real Estate goals. There will continue to be change, and it will be interesting to evaluate it each week as it is happening. I know I am trying to focus on all of the many “Silver Linings” that exist. Here’s a few tips from Windermere to help us all stay in a good state of mind during this time of uncertainty.

Please contact me with your questions and concerns, I am committed to help keep you informed!

Best Wishes!